Engagement Ring Monthly Payments: $50, $100, and $200/Month Math

Most rings are bought on a budget that lives in monthly-payment terms, not in sticker-price terms. “What can I afford?” usually means “what does the monthly look like, and how long does it last?” The answer depends almost entirely on three numbers in the financing contract: the down payment, the APR, and the minimum payment formula.

This article walks through what an engagement ring actually costs at $50, $100, and $200 a month at the financing terms used on the MJC Card from Monetary Jewelers (34% down, 19.90% APR, minimum payment 7% of the original amount financed or $50 whichever is greater, no early-payoff penalty). Each scenario shows the down payment, the financed amount, the fixed minimum, a smart pay-ahead amount, the months to payoff, and the total interest. The same math is then compared against the two financing structures most buyers see at competing stores: deferred-interest store cards and lease-to-own.

At MJC Card terms, $50 a month buys a ring around $1,000. $100 a month comfortably handles a ring up to about $2,500. $200 a month covers a ring up to about $4,000 if you pay slightly more than the minimum and clear the balance inside two years.

If your credit score is part of the decision, pair the payment math here with our guide to the best engagement-ring options for bad credit.

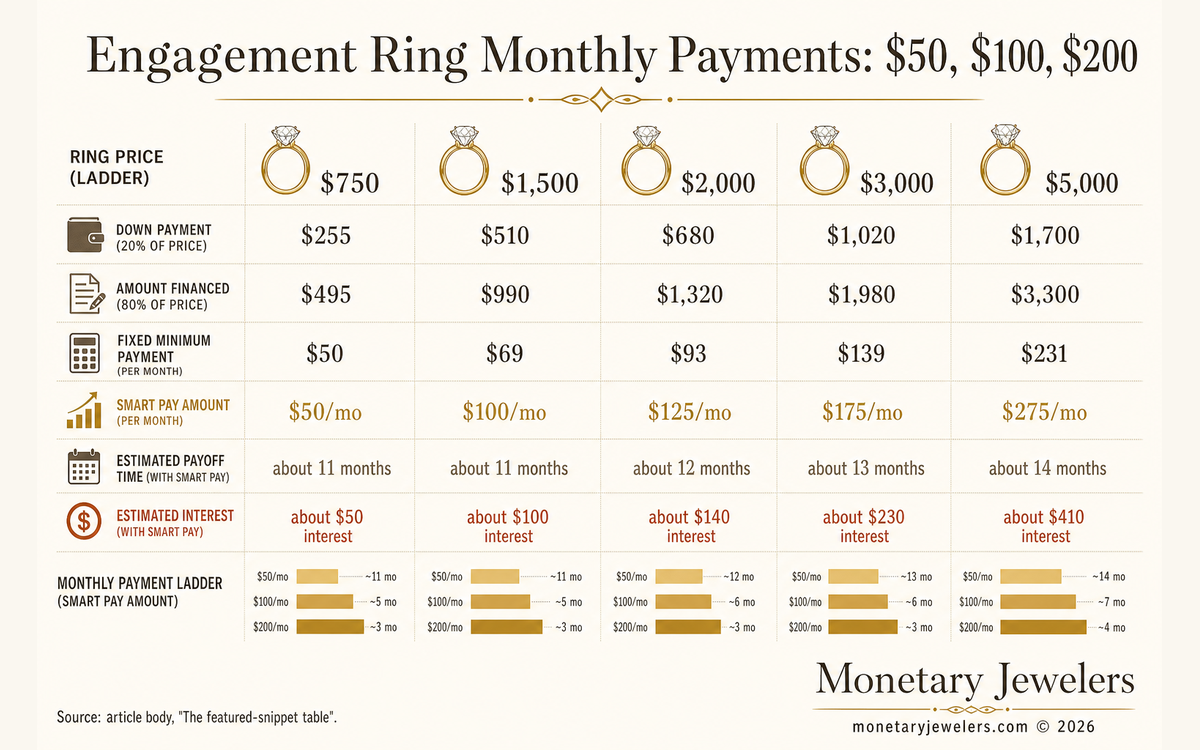

The featured-snippet table: ring price, down, financed, monthly, total

| Ring price | Down (34%) | Financed | Fixed minimum | Smart pay | Months to payoff | Total interest |

|---|---|---|---|---|---|---|

| $750 | $255 | $495 | $50 | $50/mo | ~11 | ~$50 |

| $1,000 | $340 | $660 | $50 | $75/mo | ~10 | ~$60 |

| $1,500 | $510 | $990 | $69 | $100/mo | ~11 | ~$100 |

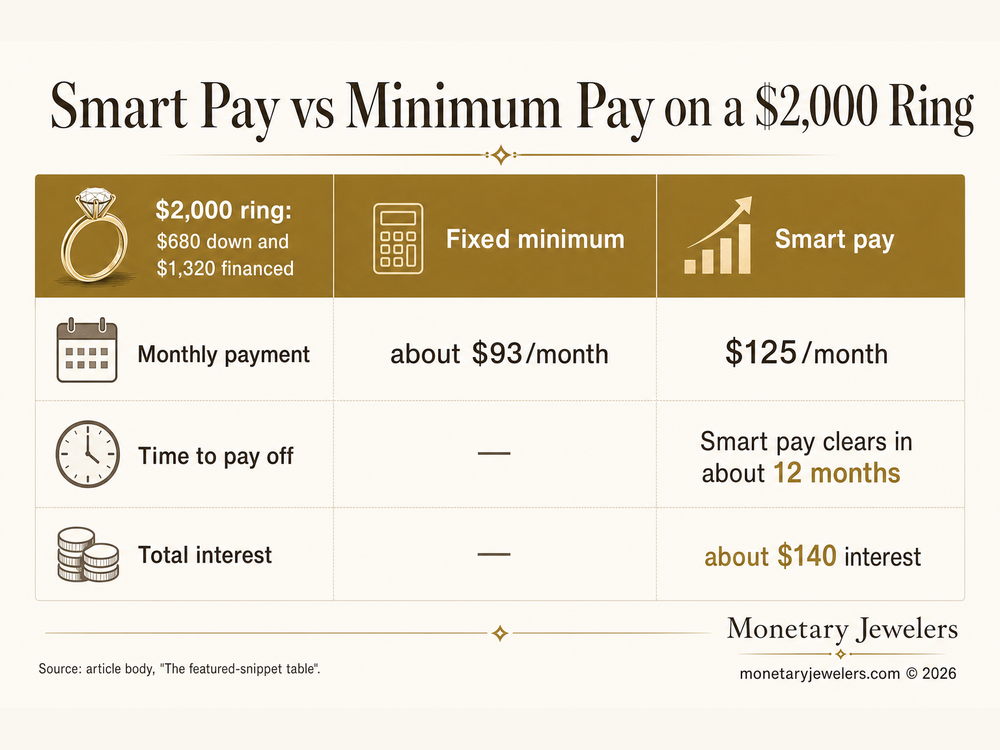

| $2,000 | $680 | $1,320 | $93 | $125/mo | ~12 | ~$140 |

| $2,500 | $850 | $1,650 | $116 | $150/mo | ~13 | ~$190 |

| $3,000 | $1,020 | $1,980 | $139 | $175/mo | ~13 | ~$230 |

| $4,000 | $1,360 | $2,640 | $185 | $225/mo | ~14 | ~$320 |

| $5,000 | $1,700 | $3,300 | $231 | $275/mo | ~14 | ~$410 |

All figures use the MJC Card published terms. “Smart pay” is the monthly amount that clears the financed balance inside roughly a year, which keeps total interest in a normal range. Paying above the fixed minimum shortens the payoff window and reduces total interest.

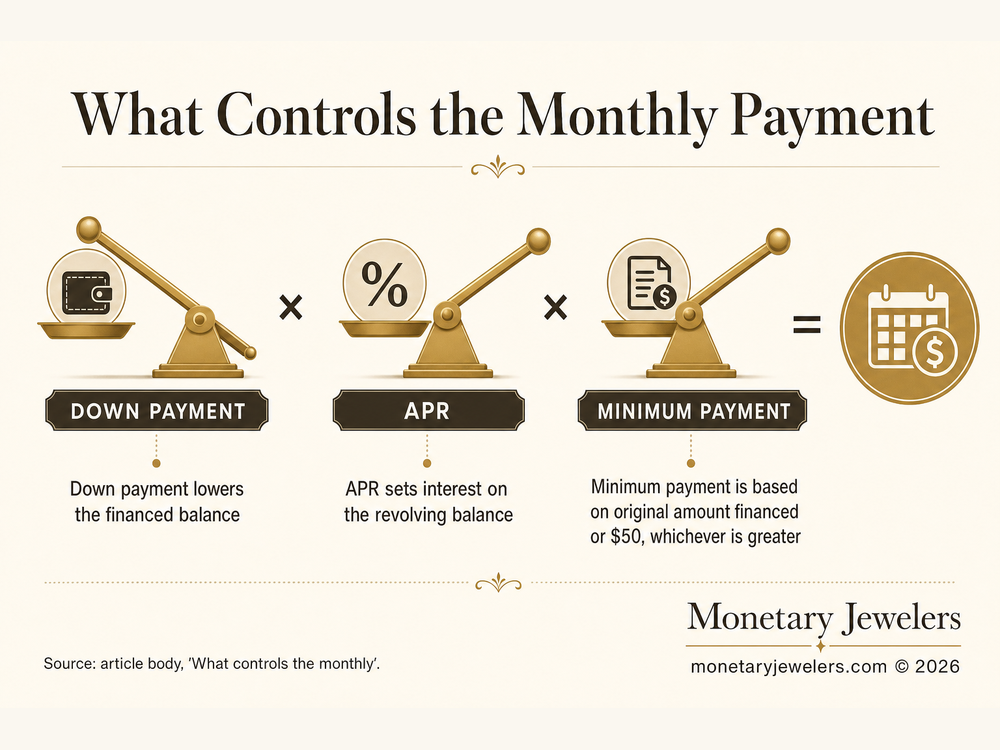

What controls the monthly: down, APR, minimum-payment formula

The monthly payment isn’t a single number set by the price of the ring. Three contract terms move it.

Down payment

A down payment lowers the financed balance, which lowers the fixed minimum monthly payment and the amount interest accrues on. At 34% down, a $3,000 ring becomes a $1,980 financed balance, not a $3,000 financed balance. A program that requires no down payment leaves the full price on your credit line, which means a higher monthly and more total interest paid even at the same APR. The monthly looks lighter at no-down-payment stores in the marketing copy, then gets heavier across the life of the contract.

APR

APR is the cost of carrying a balance. At 19.90% APR, a $1,980 financed balance accrues about $33 in interest in the first month if you pay the minimum. At 26.99% (a typical mall-jewelry store-card APR), the same balance accrues about $45 in interest in the first month. At 29.99% (the upper end of store-card APRs), it’s about $50. The first-month gap looks small. Across 18 months at minimum payments it compounds into hundreds of dollars. The Consumer Financial Protection Bureau’s Issue Spotlight on retail credit cards (2024) found that over 90 percent of retail credit cards carry maximum purchase APRs above 30 percent.

Minimum-payment formula

Most revolving credit accounts use a percentage formula with a floor. The MJC Card uses a fixed minimum of 7% of the original amount financed or $50, whichever is greater. A different formula, say 3% of the current balance with a $25 floor, looks cheaper per month and can stretch repayment significantly longer, which means more total interest. Lower minimums are not always friendlier. They often mean the lender collects more interest over the life of the account, not less.

Walking through the three scenarios

Three buyers, three monthly budgets, three ring choices. Same MJC Card terms across all three.

The $50-a-month buyer: a ring around $750 to $1,000

At MJC Card terms, the $50 minimum floor controls anything financed under about $714. A $750 ring puts $255 down, finances $495, and the minimum sits at the $50 floor for the entire contract. Pay the $50 minimum and the ring is paid off in about 11 months with around $50 of total interest. Pay $75 a month and it’s done in about 7 months with around $30 of interest.

A $1,000 ring puts $340 down, finances $660, and the fixed minimum is still $50 (because 7% of $660 is $46.20, below the floor). Same payoff window if you pay $75 a month, slightly more interest because the starting balance is larger.

This is the scenario where minimum-only payment is reasonable. Total interest stays small because the balance is small.

The $100-a-month buyer: a ring around $1,500 to $2,500

A $2,000 ring is the canonical case at this budget. Down payment $680, financed amount $1,320, fixed minimum $93. Pay the minimum and the ring is done in about 17 months with around $200 in total interest. Pay $125 a month and the ring is done in about 12 months with around $140 in interest.

A $2,500 ring at the same $100 monthly budget pushes the math harder. The fixed minimum is $116, so $100 a month is below the required payment. The buyer either chooses a slightly less expensive ring, increases the monthly to $125, or puts a larger down payment in to keep the fixed minimum below $100.

The lesson: at the $100-a-month budget, a $2,000 ring is comfortable and a $2,500 ring requires either a bigger down payment or a slightly higher monthly. The featured-snippet table makes the choice visible.

The $200-a-month buyer: a ring around $3,500 to $4,000

A $4,000 ring puts $1,360 down, finances $2,640, and runs a fixed minimum of $185. Pay $225 a month and the ring is done in about 14 months with around $320 in total interest. Pay only the fixed minimum and the same balance is done in about 17 months with around $400 in total interest.

A $5,000 ring requires a $275 monthly to clear the balance inside 14 months, which is above the $200 budget. Either the buyer raises the monthly slightly, picks a $4,000 ring, or accepts a longer payoff at $200 a month.

At every budget, the same pattern holds. Paying above the fixed minimum lowers total interest and shortens the payoff window.

Where the math goes wrong: deferred interest and lease-to-own

The featured-snippet math above only works on a transparent, simple-monthly contract. Two of the most common financing structures at competing jewelry stores quietly change the rules.

Deferred-interest store cards

A deferred-interest promotion (“0% APR for 12 months” or “6 months no interest”) doesn’t waive the interest. It defers it. If the full balance isn’t paid off by the promo’s end date, the card charges back the entire interest from the original purchase date at the regular APR (often 26.99% to 29.99%). On a $3,000 ring carried six days past the deadline, that retroactive charge can be $400 to $500 added to the balance overnight. The Consumer Financial Protection Bureau’s Issue Spotlight on retail credit cards (2024) found that about one in five deferred-interest promotional balances ends in a retroactive interest charge.

The featured-snippet table doesn’t apply on a deferred-interest contract. The “monthly payment” the store quotes is whatever clears the balance by the promo deadline, not a true minimum payment. Miss by a month and the math turns into a different problem.

Lease-to-own contracts

Lease-to-own ($89-down-and-take-it-home programs at Progressive Leasing, Acima, Snap Finance) are not financing. They are rental agreements with a buyout clause. The “monthly payment” on a lease-to-own contract is a rental fee, not a loan payment. Lease-to-own plans typically cost substantially more than the cash price of the item by the time the lease completes. In the Federal Trade Commission’s 2020 enforcement action against Progressive Leasing, which required a $175 million settlement, the FTC found consumers “frequently paid approximately twice the sticker price” under Progressive’s plans. Costs vary by provider.

A $2,000 ring at $100 a month for 24 months on a lease-to-own contract often totals $2,400 to $4,000 paid, depending on the early-buyout price and the lessor. None of those payments are reported to the credit bureaus on positive payment behavior. The featured-snippet table above does not represent the math on a lease.

How to compare an offer to this table

Three numbers tell you whether the offer you’ve been quoted matches the math above.

- The down payment, expressed as a percent of the cash price.

- The APR, expressed as an annual rate (not “no interest if paid in 12 months”).

- The minimum-payment formula, including whether the percentage is based on the original amount financed or the current balance.

If the financing page won’t tell you any of those three, the offer isn’t a transparent simple-monthly contract. That doesn’t make it a bad deal. It makes it a different kind of deal. The featured-snippet math above doesn’t apply to it. For a store-by-store lens on these approval paths, see our no-credit-check jewelry financing guide.

Why the MJC Card uses the math it uses

The MJC Card from Monetary Jewelers uses the simple-monthly structure deliberately. Eligibility and approval are subject to the MJC Card agreement and application process. Please review the current agreement before applying. Once approved, purchases are financed through a revolving credit line, and the outstanding balance carries a fixed APR of 19.90%. The minimum monthly payment is 7% of the original amount financed or $50, whichever is greater. There is no set payoff period and no prepayment penalty.

Payment activity is reported monthly to the credit bureaus. Lenders that report to the credit bureaus are subject to the Fair Credit Reporting Act (FCRA, 15 U.S.C. § 1681s-2), which requires furnishers to report accurately and to investigate disputes. The featured-snippet math above and the credit-history math both happen on the same account. The buyer who’s clearing a $1,500 ring at $100 a month gets 11 to 12 monthly statements logged as on-time payment history across every credit report a future lender might pull. That’s the design.

The math in this article only works on a contract that’s actually structured this way. Browse the engagement ring selection at the Monetary Jewelers shop to see prices, then plug them into the table above to see what each ring looks like at $50, $100, or $200 a month.

Frequently asked questions

What’s the lowest monthly payment on the MJC Card?

The minimum monthly payment is fixed at 7% of your original amount financed or $50, whichever is greater. So $50 a month is the floor for any original financed amount up to about $714. Above that, the fixed minimum scales with the original amount financed.

How much engagement ring can I get at $100 a month?

At MJC Card terms, $100 a month comfortably covers a ring up to about $2,500. A $2,000 ring runs a fixed minimum of about $93, so $100 a month sits above the minimum from day one and clears the balance in about 12 months at $125 a month if you pay slightly ahead.

What’s a $200/month engagement ring at the MJC Card?

A ring in the $3,500 to $4,000 range. A $4,000 ring puts $1,360 down and finances $2,640, with a fixed minimum of $185. Paying $225 a month clears the balance in about 14 months. A $5,000 ring requires closer to $275 a month to clear inside 14 months, which is above the $200 budget.

Does paying the minimum cost more than paying ahead?

Yes. At 19.90% APR with a fixed 7% of the original amount financed or $50 minimum-payment formula, paying only the minimum costs more than paying ahead. On a $2,000 ring, paying only the fixed minimum runs about 17 months and roughly $200 in total interest. Paying $125 a month instead clears the balance in about 12 months with around $140 in interest.

Is there a penalty for paying off the MJC Card early?

No. The MJC Card has no early-payoff penalty. You can clear the balance ahead of schedule with no extra charge.

Does financing through the MJC Card build credit?

Yes. Payment activity on the MJC Card is reported monthly to the credit bureaus. On-time monthly payments contribute to the payment-history portion of your credit profile across every credit report a future lender might pull. See the longer answer on which jewelry financing programs actually build credit at Does Jewelry Financing Build Credit? and the bureau-coverage breakdown at The 3 Credit Bureaus and Which Jewelry Financers Report.

Why do mall-store credit cards quote a lower monthly?

Many mall-store cards quote a lower monthly because they use a smaller percent-of-balance minimum (often 2% or 3%) or a deferred-interest promotion that quotes the payment needed to clear the balance by the promo deadline. The lower monthly is real, but it usually comes with either a longer payoff window (more total interest) or a retroactive interest charge if the deferred-interest deadline is missed.

Can I see the rings in the price ranges in this article?

Yes. Browse the Monetary Jewelers shop to filter engagement rings by price. Most rings between $750 and $5,000 are eligible for MJC Card financing at the terms in the table.