Does jewelry financing build credit? Here’s how to tell before you buy

If you’re financing a ring and trying to build your credit at the same time, you’re asking one purchase to do two things. Most jewelry financing programs only handle the first. Some leave your credit file in the same shape it was in before you walked into the store, and a few make it worse.

A jewelry financing plan only builds your credit if the lender reports your payment activity to the credit bureaus. Most don’t. The ones that do often report only when something goes wrong. Knowing which kind you’re applying for is the difference between two years of on-time payments showing up on your credit history and two years of payments that nobody but the store ever sees.

This guide covers what “builds credit” actually means at the level of how a credit file works, the four kinds of jewelry financing and what each one does to your credit profile, five questions you can answer in five minutes from any financing page, and an honest list of what jewelry financing will not do.

The short answer: it depends on whether the lender reports your payments

Credit bureaus build your credit history out of one thing: information that lenders send them. If a lender sends nothing, the account effectively does not exist for credit-scoring purposes, no matter how many on-time payments you make.

The single question that decides whether jewelry financing builds your credit is whether the lender reports your account activity to the major credit bureaus. A “yes” answer means the account shows up on your credit report, the age of that account contributes to the average age of your accounts, and every monthly payment becomes a piece of payment history.

A “no” answer means none of that happens. You can pay perfectly for two years and walk away with the same credit profile you started with. The ring is yours, but the credit-building part of the purchase did not exist.

A handful of programs sit in the middle. They report only adverse events (a 30-day late payment, a charge-off, a collection). On-time payments don’t appear. That kind of program can lower your score if you slip but cannot raise it if you don’t.

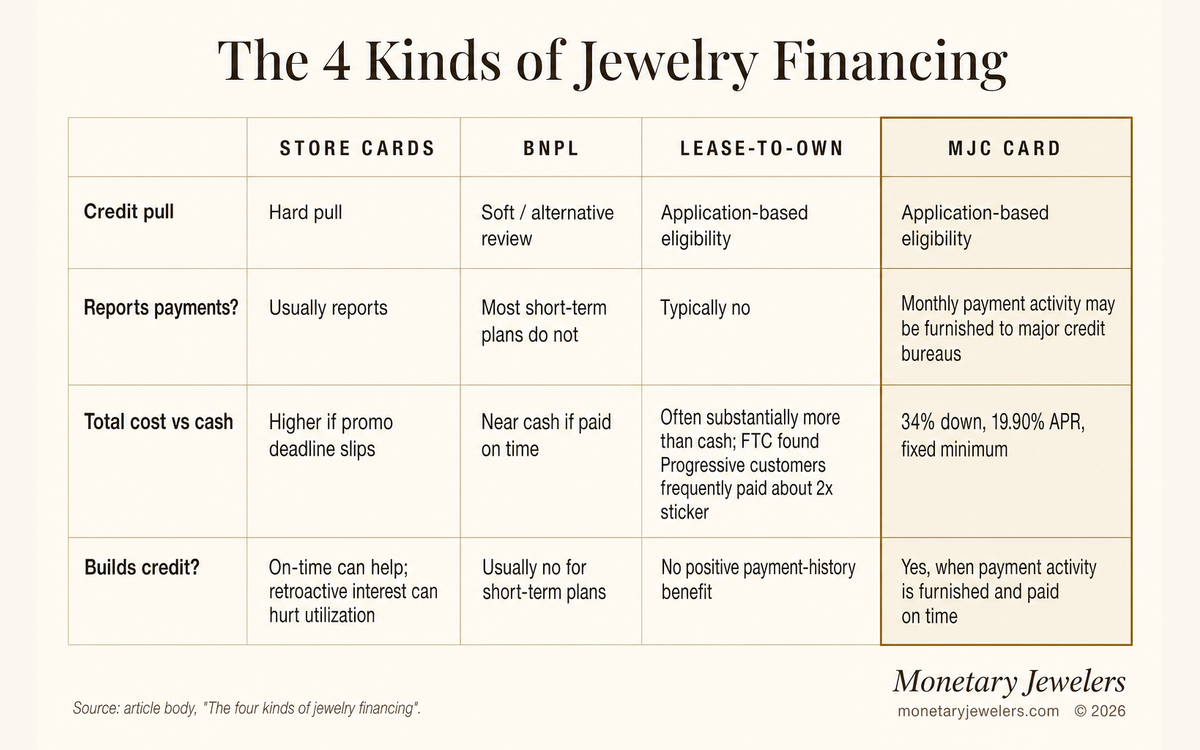

The four kinds of jewelry financing and what each one does to your credit

Almost every “finance this ring” offer falls into one of four categories. The category controls the credit-reporting behavior more than the brand or the marketing copy does.

| Financing type | Credit pull | Reports payments to credit bureaus? | Total cost vs. cash | Builds credit? |

|---|---|---|---|---|

| Traditional store credit cards (jewelry-store cards and captive lenders) | Hard pull | Yes, but the deferred-interest trap can wipe out the benefit if the payoff deadline slips | Often higher than cash if the promo deadline is missed | Yes for on-time payments; a retroactive interest charge can hurt utilization |

| Buy-now-pay-later, BNPL (Affirm, Klarna, Afterpay, Sezzle) | Soft pull | Most short-term plans do not | Roughly equal to cash if paid on time | Usually no for short-term plans |

| Lease-to-own (Progressive Leasing, Acima, Snap Finance) | Application-based eligibility | Typically no | Often substantially more than cash price (FTC’s 2020 Progressive Leasing action found roughly 2x typical) | No |

| No-credit-check financing that reports payments (MJC Card) | Application-based eligibility | Yes, to major credit bureaus monthly | Predictable at a fixed 19.90% APR | Yes |

Buy-now-pay-later (Affirm, Klarna, Afterpay, and similar)

The easiest to qualify for and almost always the lightest reporter. The provider runs a soft credit pull, approves you in seconds, and splits your purchase into a handful of installments. Most BNPL providers do not report on-time installment payments to the major credit bureaus (per the Consumer Financial Protection Bureau’s 2025 BNPL market report, which found “lenders do not typically report BNPL loans to nationwide consumer reporting companies”). A few report only the missed payments. A small number have started reporting longer-term loans, but standard short-installment plans almost never appear on your credit file when you pay on time. If credit-history building is part of why you’re financing, BNPL is rarely the right tool.

Lease-to-own (Progressive Leasing, Acima, Snap Finance)

Lease-to-own contracts are not financing in the credit-reporting sense. They are rental agreements with a buyout clause. You don’t own the ring until the lease completes, and the contract itself is a lease rather than a credit account. Most lease-to-own providers do not report on-time payments. A handful report defaults, which means lease-to-own can sometimes hurt your credit even though it can’t help it. Lease-to-own plans typically cost substantially more than the cash price of the item by the time the lease completes. In the Federal Trade Commission’s 2020 enforcement action against Progressive Leasing, which required a $175 million settlement, the FTC found consumers “frequently paid approximately twice the sticker price” under Progressive’s plans. Costs vary by provider.

Store credit cards (Kay, Zales, Jared, Daniels-style co-branded cards)

Co-branded store cards are issued by a real bank (often Comenity, Synchrony, or a similar issuer) and behave like normal credit cards on your credit report. They report balance and payment status every month and count toward your credit utilization. A low credit limit relative to a single ring purchase can push utilization high enough to lower your score even when payments are on time. Most store cards involve a hard credit pull at application and frequently come with deferred-interest promotions, where missing the payoff window by a single month retroactively applies a high annual percentage rate (APR) to the full purchase price; the deferred-interest jewelry financing guide walks through that trap in detail. The Consumer Financial Protection Bureau’s 2024 Issue Spotlight on retail credit cards found that about one in five deferred-interest promotional balances ends in a retroactive interest charge, and that over 90 percent of retail credit cards carry maximum purchase APRs above 30 percent.

In-house revolving credit (the MJC Card and a small handful of similar programs)

The rarest of the four. The store itself is the lender. There’s no third-party bank issuing the card and no leasing company holding the ring’s title. Approval can be done without a hard credit pull, because the store underwrites its own customers. And because it’s a real credit account, the store can report payment activity to the credit bureaus. Whether a specific in-house program actually does the reporting is the question that matters. The Monetary Jewelers MJC Card was built around the credit-reporting piece.

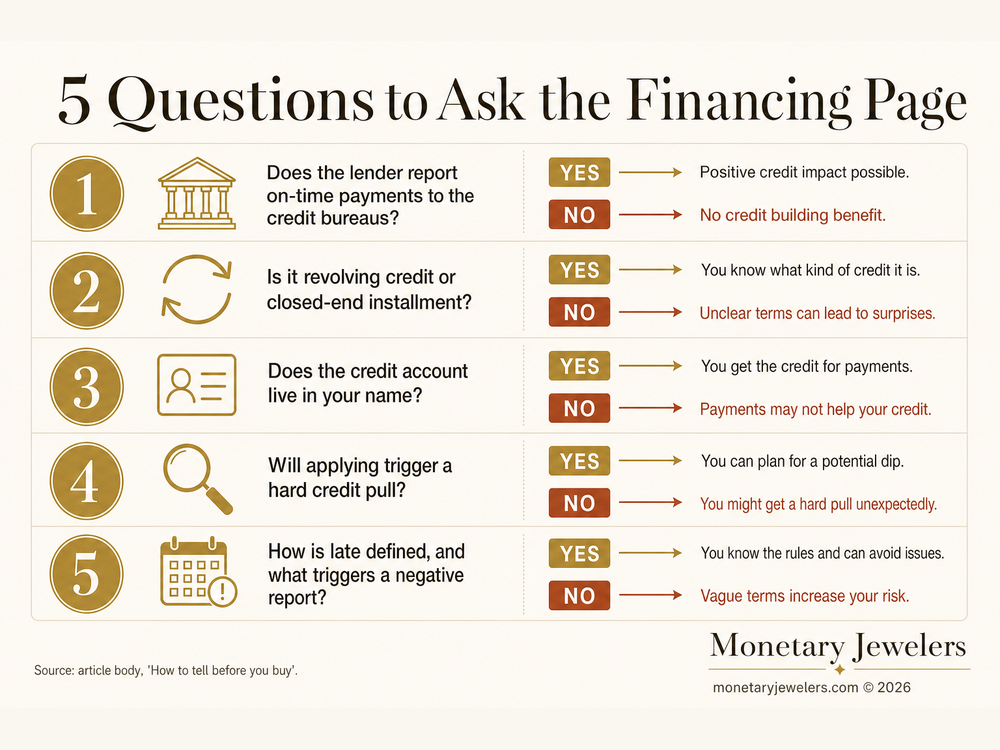

How to tell before you buy: five questions to ask the financing page

Most of these can be answered in five minutes from a store’s financing page. If a page won’t tell you, treat that silence as the answer.

Does the lender report on-time payments to the credit bureaus?

The single most important question. “We report to the credit bureaus” is not the same as “we report on-time payments.” Confirm that on-time monthly statements create positive payment-history entries, not only that the lender reports problems. If you need the bureau-by-bureau version, read the jewelry credit bureau reporting guide.

Is the account a revolving credit line or a closed-end installment loan?

Revolving accounts contribute to your credit utilization, which is one of the larger inputs in most scoring models. Installment accounts don’t. For a thin credit file, a revolving account often does more than an installment loan of the same size.

Does the credit account live in your name?

Third-party leases, layaway arrangements, and in-store credit balances often never become formal accounts in your name. Those structures cannot build credit by definition. The financing has to be opened in your name and reported under your Social Security number for it to appear on your credit file.

Will applying trigger a hard credit pull?

A hard pull temporarily lowers your score and stays on your credit report for two years. No-credit-check applications, soft-pull applications, and hard-pull applications are three different things, and most financing pages don’t say which one they’re using. Ask before you submit.

How is “late” defined, and what triggers a negative report?

Most credit accounts don’t report a late payment until it’s at least 30 days past due. Deferred-interest store cards often trigger a missed promotional window much sooner, with consequences that cost you several hundred dollars retroactively without showing up as a late mark on your credit file.

What “builds credit” actually means

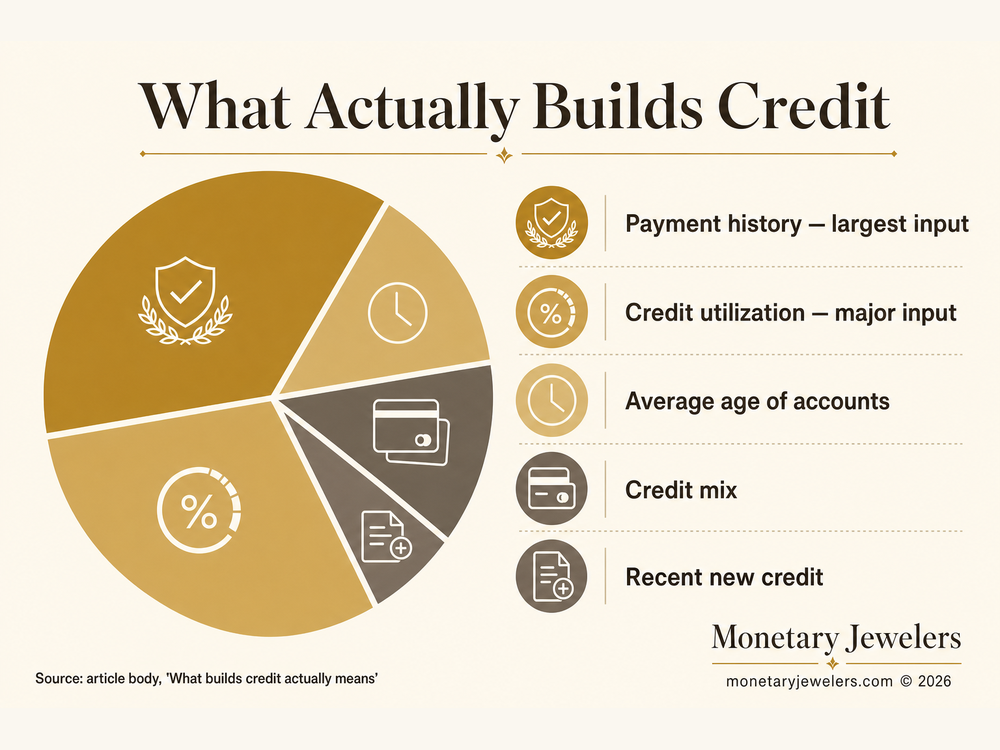

Most credit scoring models rely on five general inputs: payment history, how much of your available credit you’re using, the average age of your accounts, your mix of account types, and how much new credit you’ve recently opened. Payment history and credit utilization are the two largest inputs in most models. Lenders that report to the credit bureaus are subject to the Fair Credit Reporting Act (FCRA, 15 U.S.C. § 1681s-2), which requires furnishers to report accurately and to investigate disputes.

A new revolving account that reports on-time payments hits four of those five at once. It adds a payment-history record. It adds available credit, which improves your utilization ratio. It adds an account that, with time, raises your average account age. And it diversifies your account mix, which matters more for thin files than thick ones.

That’s the mechanism. It’s not magic, and it’s not fast. A new account typically lowers your score slightly for the first month or two before payment history starts compounding. The benefit shows up over the following 12 to 24 months as on-time payments stack up.

How the MJC Card builds credit

The Monetary Jewelers MJC Card was designed around the exact problem this article describes, where buyers want application-based jewelry financing and also want the financing itself to count toward building credit history.

Eligibility and approval are subject to the MJC Card agreement and application process. Please review the current agreement before applying. Once approved, purchases are financed through a revolving credit line, and the outstanding balance carries a fixed APR of 19.90%. The minimum monthly payment is 7% of the original amount financed or $50, whichever is greater. There is no set payoff period and no prepayment penalty.

Payment activity on the MJC Card is reported monthly to the credit bureaus. On-time payments can support payment history. Late payments are reported as well, which is what gives on-time payments meaningful weight on your credit file. Review the current agreement for reporting terms.

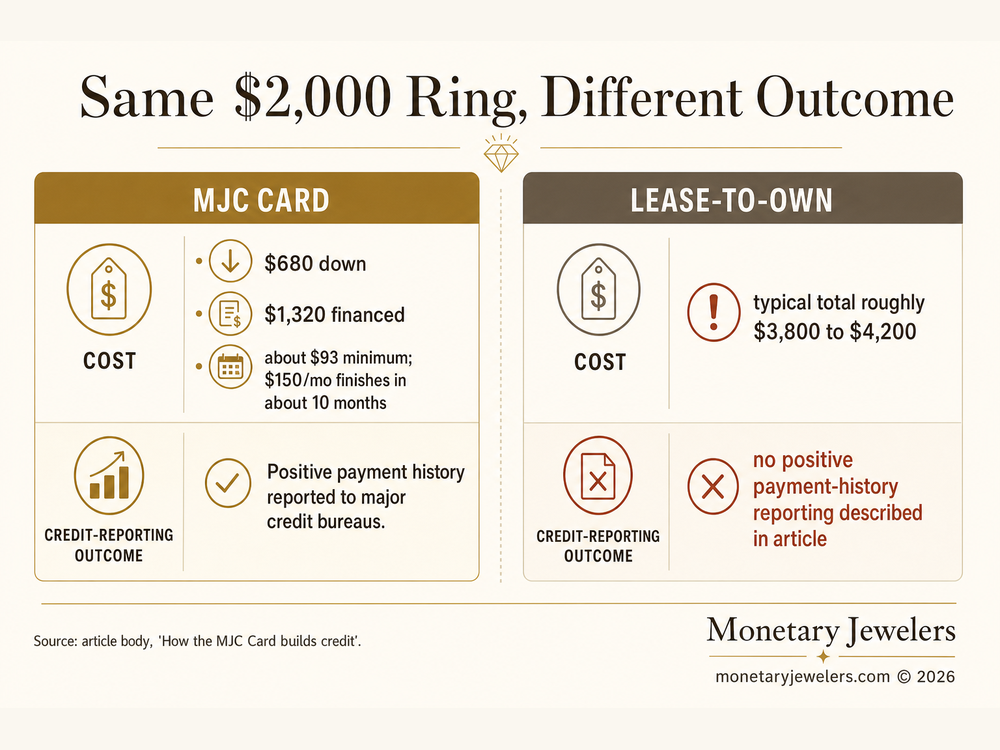

A worked example. Pick a $2,000 ring from the Monetary Jewelers shop and apply for the MJC Card. At checkout you put 34% down ($680) and finance the remaining $1,320. Your minimum payment is about $93 a month; the engagement-ring monthly payment guide shows the same math across common budgets. Pay $150 a month and you finish in about 10 months, with each of those 10 monthly statements potentially adding reported payment activity if furnished as described in the agreement. The same $2,000 ring on a typical lease-to-own contract usually runs roughly $3,800 to $4,200 total paid by the end of the lease, consistent with the FTC’s 2020 finding that Progressive Leasing customers frequently paid approximately twice the sticker price, with none of those payments contributing to your credit history.

Same ring, different financing structure, different credit outcomes.

What jewelry financing won’t do for your credit

A few honest limits.

It won’t repair items already on your credit report. Late payments, charge-offs, and collections that already exist will continue to age and fall off on the schedule the credit-reporting rules set, regardless of what you do with a new account.

It won’t help if the specific program doesn’t report. Most BNPL plans, most lease-to-own contracts, and a meaningful share of in-store credit balances don’t report on-time payments. A program that doesn’t report is not a credit-builder, regardless of how the marketing frames it.

It won’t move a thin credit file overnight. A new account drops your average account age in the first month or two, and positive payment history takes 12 to 24 months to compound into a meaningful score change.

How to start

If you’re shopping for an engagement ring specifically, the deeper bad-credit engagement ring buyer’s guide and the no-credit-check jewelry buyer’s guide walk through ring selection. If you want financing options before you pick a piece, apply for the MJC Card on the Build Your Credit page. The application takes about five minutes and shows your monthly-payment numbers before you commit to a ring; review the current agreement first so you understand eligibility review, consumer-report authorization, payment terms, and fees.

Frequently asked questions

Does Affirm build credit?

Most Affirm Pay-in-4 plans do not report to the major credit bureaus, so on-time payments on a short Affirm plan generally do not build credit history. Affirm has reported some longer-term monthly loans to one or more credit bureaus, but reporting policies vary by loan type and have shifted over time. Confirm directly with Affirm before you apply if credit-history building is part of your goal.

Does Klarna build credit?

Klarna’s standard Pay-in-4 short-term plans do not generally report on-time payments to the major credit bureaus, so they do not typically build credit history. Klarna has piloted bureau reporting on some longer-term financing products in some markets, but the reporting behavior depends on which Klarna product you’re using. Confirm with Klarna at application before assuming a plan will count toward your credit file.

Does Afterpay build credit?

Afterpay’s standard short-term installment plans do not currently report on-time payments to the major credit bureaus, so they do not generally build credit history. Late payments may be reported to bureaus or sent to collections, which means Afterpay can sometimes affect your credit negatively even when the on-time payments don’t help.

Does lease-to-own jewelry financing build credit?

Most lease-to-own programs (Progressive Leasing, Acima, Snap Finance, and similar) do not report on-time payments to the major credit bureaus, because the underlying contract is a lease rather than a credit account. They generally cannot help you build credit history, and some can affect your credit negatively if a lease defaults. Lease-to-own plans typically cost substantially more than the cash price of the item by the time the lease completes. In the FTC’s 2020 enforcement action against Progressive Leasing, which required a $175 million settlement, the FTC found Progressive customers frequently paid approximately twice the sticker price. Costs vary by provider.

Does the MJC Card build credit?

Yes. The Monetary Jewelers MJC Card is a revolving credit account, and payment activity is reported monthly to the credit bureaus. On-time payments can support payment history on your credit file, and late payments are reported as well. The MJC Card is one of the few jewelry financing programs that combines application-based eligibility with credit-bureau reporting on the same account.

How long does it take for jewelry financing to show up on my credit report?

A new credit account typically appears on your credit report within 30 to 60 days of the first statement closing, although the exact timing depends on the lender’s reporting cycle and which credit bureaus the lender reports to. Once the account appears, on-time payments compound into payment history over the following 12 to 24 months.

Can jewelry financing hurt my credit?

Yes, in two ways. A hard credit pull at application can temporarily lower your score by a few points, regardless of whether you’re approved. And if the financing reports to the credit bureaus, late payments, charge-offs, or collections on the account will appear on your credit report and can lower your score meaningfully. Programs that report only adverse events can hurt your credit but cannot help it.

What’s the difference between a hard pull and reporting to the credit bureaus?

A hard pull is a one-time event when you apply, where the lender requests your full credit report from one or more bureaus. Reporting to the credit bureaus is the ongoing process where the lender sends your account activity (balance, minimum payment status, monthly payment behavior) to the bureaus over the life of the account. A program can do one without the other. For example, the MJC Card application doesn’t require a credit pull at all but the account itself reports activity monthly once it’s open.

Does Monetary Jewelers report payments to the credit bureaus?

Yes. MJC Card account information is reported monthly to the credit bureaus. Review the current agreement for reporting terms.

Will paying off my MJC Card balance early hurt my credit?

Paying down a revolving balance generally helps your credit, because it lowers your credit utilization. Closing the account after payoff can have a small negative effect on the average age of your accounts, but most buyers leave the account open and unused after payoff to preserve the available credit and the account history. There is no early-payoff penalty on the MJC Card, so paying ahead saves interest and does not trigger any account fees.