Deferred Interest in Jewelry Financing: How a 0% APR Ring Becomes 29% APR Debt

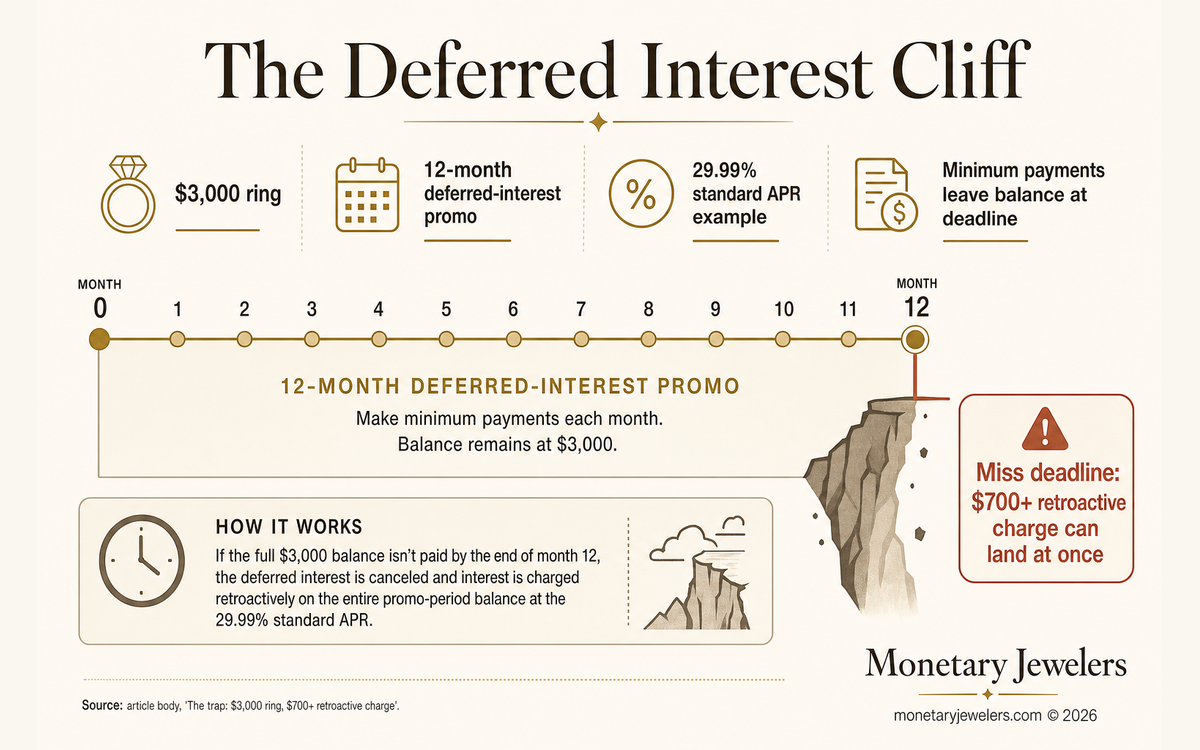

Most “0% APR” jewelry financing offers are not 0% offers. They are deferred-interest contracts. The interest accrues from the day the card is swiped, at the standard APR (often 26.99% to 29.99%). It only stays off the balance if the entire purchase is paid off by a fixed deadline. Miss the deadline by a single day or by a single dollar, and the lender adds every month of accrued interest to the balance in one charge.

This is the structure behind most jewelry-store credit cards (Kay, Zales, Jared, and the Daniels-style co-branded family) and behind many third-party promotional offers used at independent jewelers. The Consumer Financial Protection Bureau’s Issue Spotlight on retail credit cards (2024) found that about one in five deferred-interest promotional balances results in retroactive interest charges, and that over 90 percent of retail credit cards carry maximum purchase APRs above 30 percent. The math doesn’t show up on the contract. It shows up on the statement after the deadline passes, often $700 or more, on a balance the buyer thought was almost paid off.

The math is unforgiving. On a $3,000 ring at a 12-month deferred-interest promo with a 29.99% standard APR, missing the payoff deadline by even a single dollar triggers a full retroactive interest charge. Buyers who pay only the minimum during the promo are the most exposed. The article’s worked example shows this scenario costs approximately $4,500 by the time the balance clears. The same ring on a transparent simple-monthly contract clears in 13 months at about $3,230 total.

If you are comparing store-card promotions against other payment paths, review the practical engagement-ring financing options for bad credit before choosing a plan.

What deferred interest means

A deferred-interest promotion is a financing offer that waives interest only if the entire balance is paid off by a fixed deadline. It is not a 0% APR offer in the standard sense. Two short phrases on a card offer point to two completely different products.

“0% APR for 12 months”

This is a true promotional rate. Interest is calculated at 0% during the promo period. After the promo ends, only the remaining balance accrues interest at the standard APR going forward. The first 12 months are, mathematically, free. Whatever balance is left on month 13 becomes a normal credit-card balance at the regular rate.

“No interest if paid in full in 12 months”

This is deferred interest. Interest accrues from the purchase date at the standard APR for the entire 12 months. The lender doesn’t charge it to the statement during the promo window. If the balance reaches zero on or before the deadline, the accrued interest is waived in full. If a single dollar remains after the deadline, every month of accrued interest is added to the balance in a single retroactive charge.

The two phrases sound nearly identical when read off a sign at the counter. The math is not.

The trap: $3,000 ring, $700+ retroactive charge

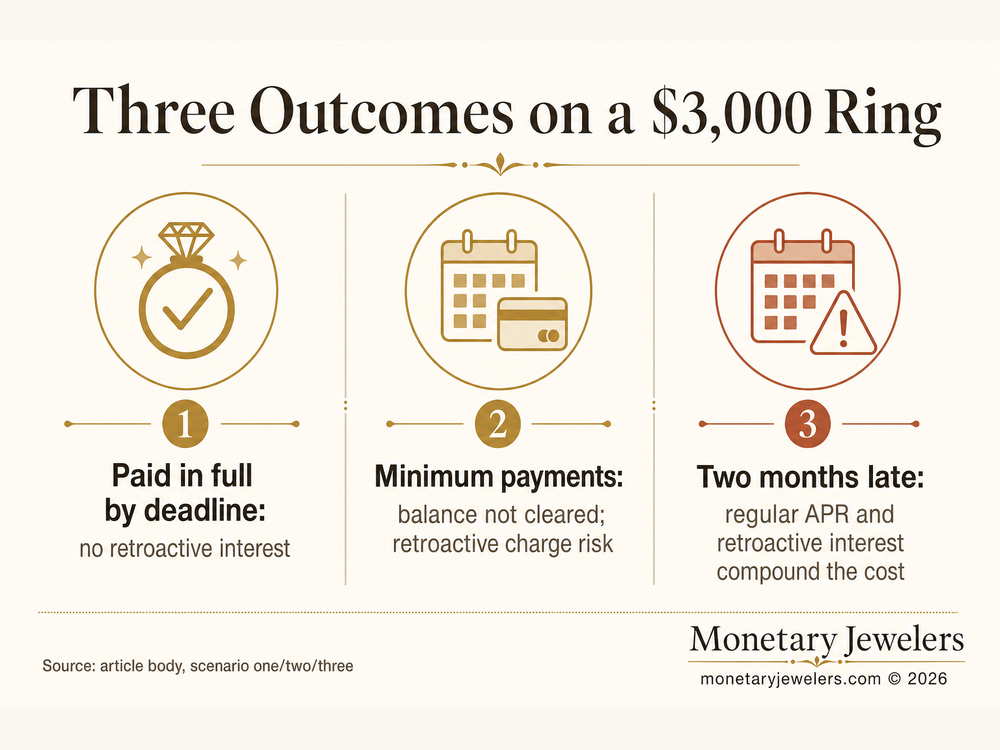

A worked example shows what is at stake.

A buyer finances a $3,000 engagement ring on a 12-month deferred-interest promo with a 29.99% standard APR (a typical standard rate for major mall-jewelry store cards, per their published cardholder terms). Minimum payment is 3% of balance or $25, whichever is greater. The buyer pays the minimum each month and assumes the deal works the same as a 0% APR loan.

Scenario one: paid in full by the deadline

The buyer pays roughly $250 a month (the amount required to clear $3,000 in 12 months at 0%). The balance hits zero in month 12. Total interest charged: $0. Total paid: $3,000. This is what the marketing implies and what a disciplined buyer with a clear payoff plan delivers.

Scenario two: minimum payments, balance not cleared at the deadline

The buyer pays the 3% minimum every month, which starts at $90 and shrinks as the balance shrinks. Across the 12 months, they pay about $920 total, leaving roughly $2,080 still on the card the day the promo ends. At that moment, the lender charges back every month of accrued interest from the purchase date (about $765 on the running balance at 29.99% APR). The new balance is $2,080 + $765 = $2,845. The “0% APR” ring took on $765 in interest in a single billing cycle.

The buyer also moves to the standard 29.99% APR going forward. Continuing at $200 a month from there, the balance clears in another 18 months with about $716 more in interest. Total cost on the $3,000 ring: about $4,520, paid across 30 months. That is the $700+ retroactive charge plus another $700+ in regular interest the deferred-interest contract collects after the promo ends.

Scenario three: paid off two months late

A buyer who realizes the trap in month 11 and rushes to clear the balance by month 14, two months past the deadline, doesn’t escape the retroactive charge. The deferred-interest waiver is binary. Even paying the balance the day after the promo ends triggers the full retroactive charge. The two-extra-months scenario costs roughly the same $765 as scenario two, plus a small amount of additional interest for the late period.

The structure is designed so that the cost of being “almost on time” is almost identical to the cost of being a year late. There is no partial-credit version of the deal.

Why store credit cards use this structure

Deferred interest exists because it works for the lender. The buyer hears “0% APR” and stretches the purchase budget. The minimum payment is set at a rate (typically 2% or 3% of balance) that mathematically cannot clear the principal inside the promo. A buyer who pays only the minimum is guaranteed to miss the deadline.

A useful number to keep in mind. On a 12-month deferred-interest promo at a 3% minimum payment, paying the minimum for the full year clears about 31% of the original purchase. The remaining 69% triggers the retroactive charge. The shortfall is not an accident in the contract. The shortfall is the contract.

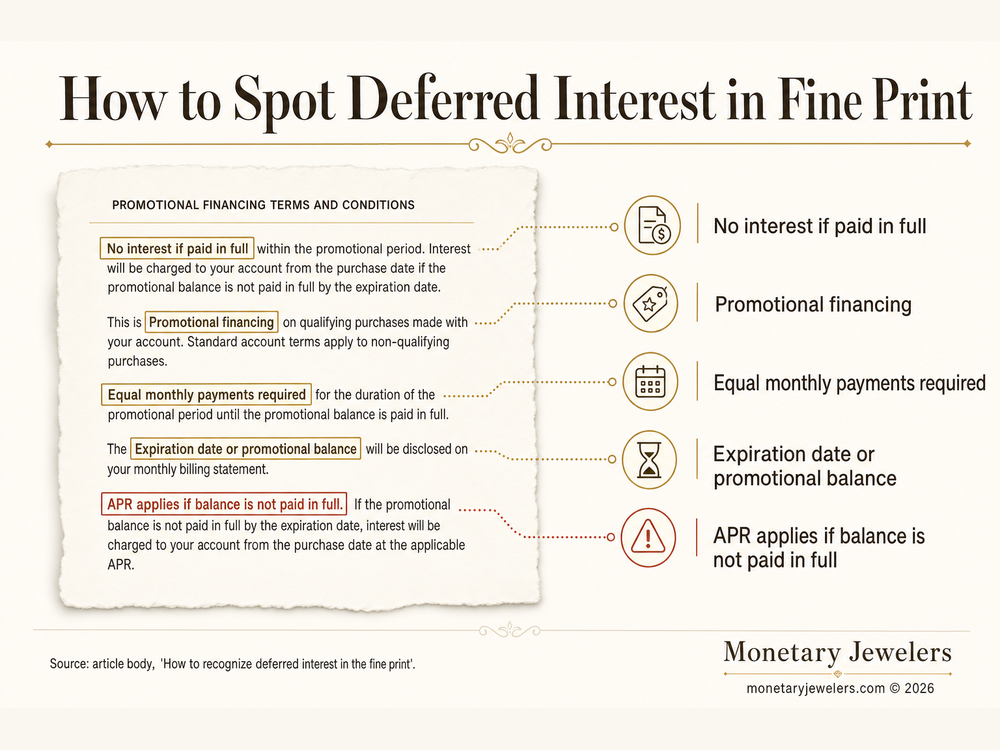

How to recognize deferred interest in the fine print

Three phrase patterns reliably signal deferred interest in a financing offer. If any of them appears, treat the promo as deferred interest until the lender confirms otherwise in writing.

“No interest if paid in full”

The cleanest signal. Any financing offer using the phrase “no interest if paid in full” in any tense (the past, the future, the conditional) is a deferred-interest offer. Real 0% APR offers say “0% APR for X months” without conditioning the rate on payoff timing.

“Promotional financing”

The Consumer Financial Protection Bureau uses “promotional financing” as an umbrella term in its retail-credit-card research, covering deferred interest, true 0% APR, and reduced-rate offers. If a financing page only describes the offer as “promotional financing” without specifying which kind, the offer is more often deferred interest than true 0% APR. Ask the issuer directly.

“Equal monthly payments required”

A small number of lenders use this phrase to describe a true installment loan with a fixed payment schedule, in which case the offer is not deferred interest at all. Most lenders use it to describe the payment that would clear the balance by the promo deadline, which means missing that schedule triggers the retroactive charge. Read the next sentence of the disclosure carefully. If it mentions interest accruing from the purchase date, the offer is deferred interest.

How to read a deferred-interest statement

Once a deferred-interest account is open, the monthly statement usually shows two relevant numbers in addition to the regular balance. The first is the promotional balance, which is the amount remaining on the deferred-interest portion of the account. It has to reach zero by the deadline. The second is the promotion expiration date, which is the day the lender checks whether the promotional balance is zero.

If the promotional balance is not zero on the day after the expiration date, expect the retroactive charge on the next statement. Some issuers also disclose the unpaid accrued interest as a running total on each statement, which makes the trajectory easier to see in advance.

The simple-monthly alternative: how the MJC Card is structured

The MJC Card from Monetary Jewelers is designed without deferred interest. The contract terms are stated upfront and stay in place for the life of the account.

| Financing type | Credit pull | Reports payments to credit bureaus? | Total cost vs. cash | Builds credit? |

|---|---|---|---|---|

| Traditional store credit cards (jewelry-store cards and captive lenders) | Hard pull | Yes, but the deferred-interest trap can wipe out the benefit if the payoff deadline slips | Often higher than cash if the promo deadline is missed | Yes for on-time payments; a retroactive interest charge can hurt utilization |

| Buy-now-pay-later, BNPL (Affirm, Klarna, Afterpay, Sezzle) | Soft pull | Most short-term plans do not | Roughly equal to cash if paid on time | Usually no for short-term plans |

| Lease-to-own (Progressive Leasing, Acima, Snap Finance) | Application-based eligibility | Typically no | Often substantially more than cash price (FTC’s 2020 Progressive Leasing action found roughly 2x typical) | No |

| No-credit-check financing that reports payments (MJC Card) | Application-based eligibility | Yes, to major credit bureaus monthly | Predictable at a fixed 19.90% APR | Yes |

The lease-to-own row above reflects the Federal Trade Commission’s 2020 enforcement action against Progressive Leasing, which required a $175 million settlement and found consumers “frequently paid approximately twice the sticker price” under Progressive’s plans. Costs vary by provider.

Eligibility and approval are subject to the MJC Card agreement and application process. Please review the current agreement before applying. Once approved, purchases are financed through a revolving credit line, and the outstanding balance carries a fixed APR of 19.90%. The minimum monthly payment is 7% of the original amount financed or $50, whichever is greater. There is no set payoff period and no prepayment penalty. There is no promotional period. There is no expiration date. There is no retroactive charge.

The same $3,000 ring example, run on MJC Card terms instead of a deferred-interest store card. Down payment at 34% is $1,020. Financed balance is $1,980. The fixed minimum is $138.60. Paying $175 a month clears the balance in about 13 months with around $230 in total interest. Total cost on the $3,000 ring: about $3,230, paid across 13 months.

Compared to the deferred-interest scenario two above, the simple-monthly path saves roughly $1,290 of total interest and 17 months of repayment time on the same $3,000 ring. The MJC Card also may furnish payment activity to major credit bureaus, which gives the buyer a transparent payoff schedule and a positive payment history that shows up on every credit report a future lender pulls. The deferred-interest path adds risk to the credit profile in the months the retroactive charge inflates utilization.

How to compare an offer to this article

Three questions surface deferred-interest exposure on any financing offer before signing.

- Is the rate written as “0% APR” or as “no interest if paid in full”? The first is a true promotional rate. The second is deferred interest.

- Does the lender disclose a “promotional balance” and an expiration date? Both phrases are deferred-interest indicators.

- What APR applies if the balance is not paid in full by the promo deadline? Any answer above 0% means missing the deadline triggers a retroactive charge at that rate.

A simple-monthly contract has no answer for question 2 because there is no promotional period. The APR on day one is the APR on day 365 because the rate is fixed.

Where to start

If a 0% APR jewelry financing offer is on the table, read the financing terms again with the phrases above in mind before signing. Most major mall-jewelry store cards run on deferred interest, which means the buyer has to clear the balance by a fixed date or pay the full retroactive charge.

To skip the deferred-interest math entirely, browse engagement rings at the Monetary Jewelers shop, compare approval language in the jewelry stores no credit check guide, and price out the simple-monthly numbers using the monthly-payment math article for a $50, $100, or $200 monthly budget. The MJC Card application sits at the Build Your Credit page and takes about five minutes. Application-based eligibility, no promo deadline, no retroactive charge, and payment activity is reported monthly to the credit bureaus.

Frequently Asked Questions

Is “0% APR” the same as “deferred interest”?

No. A true 0% APR offer charges 0% interest during the promo period. A deferred-interest offer accrues interest from the purchase date at the standard APR (typically 26.99% to 29.99%) and waives that interest only if the full balance is paid by the promo’s deadline. Miss the deadline by a single day or a single dollar and the lender retroactively adds every month of accrued interest to the balance.

Do most jewelry store credit cards use deferred interest?

Yes. The major mall-jewelry store cards (Kay, Zales, Jared, and similar) and many independent-store financing partners commonly use deferred-interest promotions as their default 0% offer. Deferred interest is also the most common structure across consumer-finance “no interest” promotions in furniture, electronics, appliances, and similar categories.

What happens if I’m $1 short of paying off a deferred-interest promo on time?

The retroactive charge applies in full. Most issuers calculate the charge as the interest that accrued from the purchase date at the standard APR. On a $3,000 ring at a 12-month promo with a 29.99% standard APR, paying the minimum each month and leaving roughly $2,080 on the card at the deadline triggers approximately $765 in retroactive interest. The retroactive amount does not scale with how close the buyer came to clearing the balance.

Can I tell from the marketing whether an offer is deferred interest?

Sometimes. Deferred-interest offers usually use phrases like “no interest if paid in full” or “promotional financing.” True 0% APR offers say “0% APR for X months” without conditioning the rate on payoff timing. If the offer page is silent on which structure applies, ask the issuer for the standard APR that applies after the promo and how unpaid interest is calculated. The answer will reveal which kind of promo is in play.

Does paying the minimum on a deferred-interest promo clear the balance in time?

Usually no. Most deferred-interest cards set the minimum payment at 2% or 3% of balance, which does not clear the principal inside a 12- or 18-month promo. A buyer paying the minimum on a 12-month promo at 3% typically clears about 31% of the original purchase by the deadline. The other 69% triggers the retroactive charge. The minimum payment is set to leave a balance.

Does deferred-interest financing show up on my credit report?

Yes. The underlying card account reports normally to the credit bureaus the issuer furnishes to. On-time minimum payments build payment history. The retroactive interest charge increases the balance, which raises the credit-utilization ratio, often spiking it past 30% or even 100% of the credit limit on a smaller line. A higher utilization ratio can drop the credit score for the months the inflated balance carries. Even a deferred-interest account paid on time across the promo can have a negative net credit effect if the retroactive charge fires.

What’s the difference between deferred interest and the MJC Card?

The MJC Card uses a simple-monthly revolving structure with a fixed 19.90% APR, a 7% of the original amount financed or $50 minimum-payment formula, and no promotional period. There is no deadline to clear the balance, no retroactive charge, and no rate change. The buyer can carry the balance for as long as needed, paying interest on the actual balance each month at the same fixed rate. Total interest is predictable from day one. See the longer answer at the does jewelry financing build credit article.

How do I avoid the deferred-interest trap if I want a 0% offer?

Two checks. First, confirm the offer is a true 0% APR rather than a deferred-interest “no interest if paid in full” promo. The phrasing on the offer page is the first signal. Second, if the offer is deferred interest and the deal still looks good, calculate the monthly amount needed to clear the full balance by the deadline (the original purchase price divided by the number of promo months) and pay that amount or more every month, never the minimum. The minimum payment on a deferred-interest card is set to leave a balance at the deadline.

Can the retroactive interest charge be negotiated away?

Sometimes, in narrow circumstances. If the balance was cleared within a few days of the deadline, the issuer’s customer-service line may waive the charge as a one-time courtesy, especially for accounts in good standing. There is no contractual right to a waiver. The retroactive charge is enforceable as written. Treat the deadline as a hard line, not a guideline.

Does the MJC Card report payments to credit bureaus?

Yes. The MJC Card may furnish payment activity to major credit bureaus. On-time payments can support payment history across every credit report a future lender pulls. See the bureau-coverage breakdown for how the three bureaus differ and why all-three reporting matters.