Jewelry stores that finance can make a larger engagement ring, wedding band, gold chain, or fine-jewelry purchase easier to plan. The hard part is that every store uses different language. One jeweler may offer a store credit card, another may route shoppers to a third-party lender, another may advertise buy now pay later, and another may use lease-style financing. Monetary Jewelers offers the MJC Card, an in-house revolving credit account for eligible jewelry purchases of $1,500 or more. The MJC Card uses application-based eligibility, 34% down, 19.90% APR, a fixed minimum-payment formula, no prepayment penalty, and payment activity is reported monthly to credit bureaus.

What to Look for in Jewelry Stores With Financing

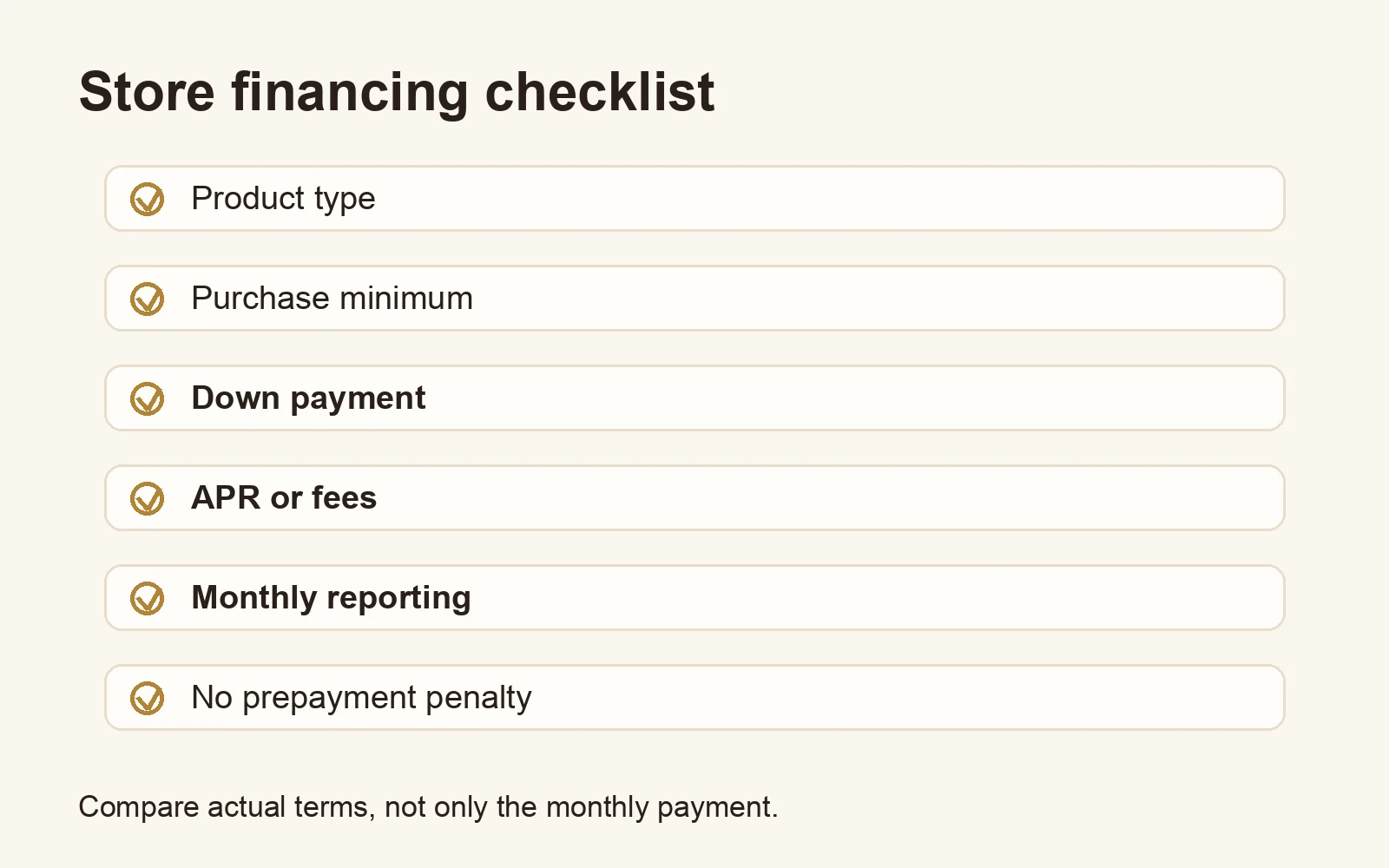

The right jewelry store financing option should be understandable before you apply. Do not compare only the monthly payment. Compare the product type, total cost, down payment, APR or fees, payoff flexibility, reporting behavior, and what happens if you are late. A low advertised payment is not useful if the agreement hides ownership timing, deferred-interest risk, or unclear fees.

Use this checklist when comparing jewelry stores that finance:

- Is the offer store credit, a personal loan, BNPL, lease-to-own, or a revolving account?

- What purchase amount qualifies?

- How much is required down?

- What APR or fee structure applies after checkout?

- How is the minimum monthly payment calculated?

- Can you pay early without a prepayment penalty?

- Does the account report payment activity monthly to credit bureaus?

- Is approval clearly described as conditional rather than guaranteed?

How Monetary Jewelers Financing Works

Monetary Jewelers is a jewelry store with in-house financing through the MJC Card. The account is for Monetary Jewelers purchases, not general cash use, and it is not a personal loan or lease-to-own contract. The terms are designed to be clear at the point of comparison:

- Eligible purchases start at $1,500

- 34% down

- 19.90% APR

- Minimum monthly payment of $50 or 7% of the original amount financed, whichever is greater

- No prepayment penalty

- Payment activity is reported monthly to credit bureaus

- Approval is not guaranteed

This structure matters because a shopper can compare Monetary Jewelers against other jewelry stores with financing using the same questions: how much is due today, what is financed, how payments are calculated, whether the account reports, and whether paying early is allowed.

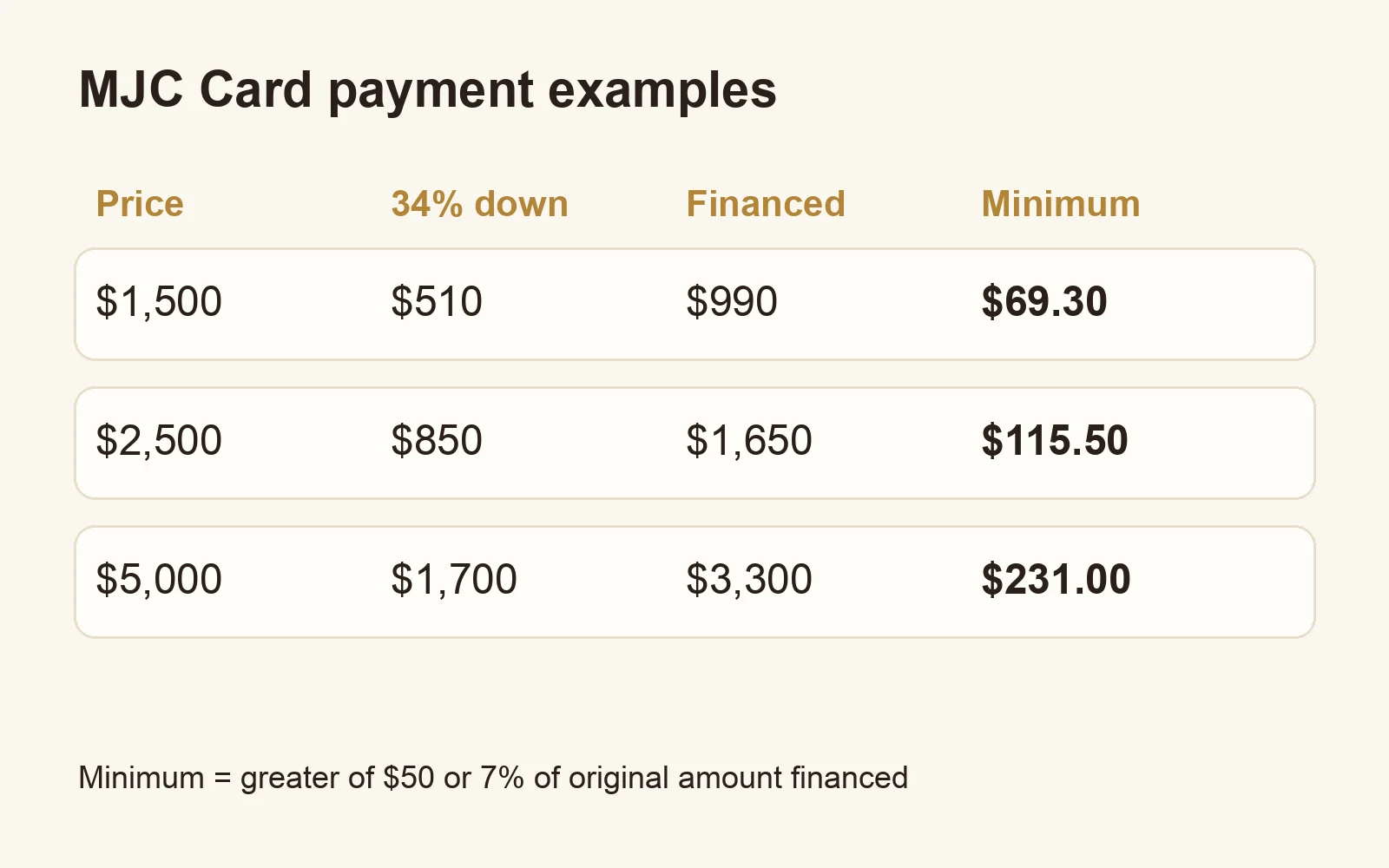

Payment Examples at Common Jewelry Prices

The MJC Card requires 34% down. The financed amount is the purchase price minus the down payment, and the minimum monthly payment is the greater of $50 or 7% of the original amount financed. Examples:

| Purchase price | 34% down | Amount financed | Minimum monthly payment |

|---|---|---|---|

| $1,500 | $510 | $990 | $69.30 |

| $2,500 | $850 | $1,650 | $115.50 |

| $5,000 | $1,700 | $3,300 | $231.00 |

Interest accrues at 19.90% APR on any carried balance. There is no prepayment penalty, so paying more than the minimum can reduce total interest and shorten the payoff timeline. For the full hub, see jewelry financing. For ring-specific shopping, see engagement ring financing.

Shop Finance-Eligible Jewelry

MJC Card eligibility can be considered for qualifying jewelry purchases of $1,500 or more. These product rails are filtered to show pieces above that minimum:

Browse by category: engagement and wedding rings, fine jewelry rings, necklaces and pendants, bracelets, earrings, and men’s jewelry.

In-House Financing vs. Third-Party Financing

In-house financing means the jewelry store is directly involved in the account or financing relationship. The advantage is fit: the financing is built around the jewelry purchase, not a general-purpose cash loan. The MJC Card is an in-house Monetary Jewelers account for jewelry purchases. Stores built around this model are often called credit jewelers — see what a credit jeweler is and how these accounts report.

Third-party financing can include BNPL apps, lease-to-own providers, store-card partners, and personal-loan lenders. These can work for some shoppers, but the terms are controlled by the provider. Review the application impact, reporting behavior, and total cost before you choose.

Promotional financing can be attractive when the promotion is real and you can pay within the promotional window. The risk is deferred interest or a missed deadline that changes the cost. If you are comparing promotions, read the deferred-interest jewelry financing guide.

BNPL for jewelry may be simple for smaller purchases, but short-term plans vary in reporting and payoff rules. For that comparison, see buy now pay later jewelry. For lease-style offers, see lease-to-own jewelry.

Jewelry Stores That Finance Near Me or Online

Searches for “jewelry stores that finance near me” and “jewelry stores with financing online” usually come from the same need: the shopper has found a piece they want and needs a payment path that is clear. Local stores may offer personal relationships and in-person guidance. Online jewelry stores may offer more inventory and faster comparison. Either way, the financing terms are what decide whether the offer fits.

Monetary Jewelers lets shoppers browse online and apply for the MJC Card through the same site. If approved, the MJC Card can be used for eligible Monetary Jewelers purchases with the terms listed above. If your search is specifically about credit-check wording, use the companion page on no credit check jewelry financing for safer definitions and comparisons.

When the MJC Card May Fit

The MJC Card may fit shoppers who want a jewelry-store financing account with known terms, monthly payment reporting, and no prepayment penalty. It may also fit shoppers comparing jewelry stores that finance because the down payment, APR, and minimum payment formula are stated up front.

It will not fit every shopper. The purchase must meet the $1,500 eligibility minimum, 34% down is required, interest applies to carried balances, and approval is not guaranteed. The best next step is to compare the jewelry you want, the down payment you can make, and the payoff pace you can sustain. If another store advertises “guaranteed approval,” read what guaranteed jewelry financing really means before relying on it.

How to Apply

- Choose a jewelry piece or category you want to compare.

- Review the MJC Card terms: 34% down, 19.90% APR, fixed minimum payment, no prepayment penalty, and monthly payment-activity reporting.

- Apply through the MJC Card application page.

- If approved, complete the purchase with 34% down and finance the remaining balance on the MJC Card.

- Pay the fixed minimum or more each month; paying above the minimum can reduce total interest and payoff time.

Frequently Asked Questions

Does Monetary Jewelers finance jewelry?

Yes. Monetary Jewelers offers MJC Card financing for eligible jewelry purchases of $1,500 or more. The MJC Card is an in-house revolving credit account for Monetary Jewelers purchases.

What are the MJC Card terms?

The MJC Card uses application-based eligibility, 34% down, 19.90% APR, and a minimum monthly payment of $50 or 7% of the original amount financed, whichever is greater. There is no prepayment penalty.

Is every application approved?

No. Approval is not guaranteed. Eligibility is application-based, so shoppers should review the terms before applying.

Does the MJC Card report payments?

Yes. MJC Card payment activity is reported monthly to credit bureaus. On-time payments can support payment history over time, while late payments can hurt it. No credit-score outcome can be promised.

What is the minimum purchase for MJC Card financing?

The minimum eligible jewelry purchase for MJC Card financing is $1,500.

Can I pay off MJC Card financing early?

Yes. The MJC Card has no prepayment penalty. Paying more than the minimum can reduce total interest and shorten the payoff timeline.