Buy now pay later jewelry plans split a jewelry purchase into payments instead of requiring the full price upfront. At Monetary Jewelers, the buy-now-pay-later path is the MJC Card: an in-house revolving credit account with application-based eligibility and clear terms before you apply. This page explains how buy now pay later jewelry works, how it differs from app-based BNPL providers, the real MJC Card payment math, and when a reported in-house account may be a better fit than a short-term installment app.

How Buy Now Pay Later Jewelry Works

Most buy now pay later jewelry offers fall into four buckets: short-term BNPL apps, store credit cards, personal loans, and in-house revolving accounts. The words can sound interchangeable, but the contract underneath matters. A four-payment app can be useful for a small purchase you can clear quickly. A store card may work for shoppers with strong credit and a promotional window. A personal loan may fit a larger purchase if the rate is competitive. The MJC Card is different: it is an in-house revolving account issued by Monetary Jewelers with application-based eligibility.

The MJC Card terms are straightforward:

- Application-based eligibility

- Minimum jewelry purchase for MJC Card financing is $1,500

- 34% down

- 19.90% APR

- Minimum monthly payment of $50 or 7% of the original amount financed, whichever is greater

- No prepayment penalty

- Monthly payment activity is reported monthly to credit bureaus

The fixed-minimum structure is the key difference from many general-purpose cards. Your minimum is based on the original amount financed, so you know the payment floor before you commit. Paying more than the minimum shortens the payoff and reduces total interest, with no prepayment penalty.

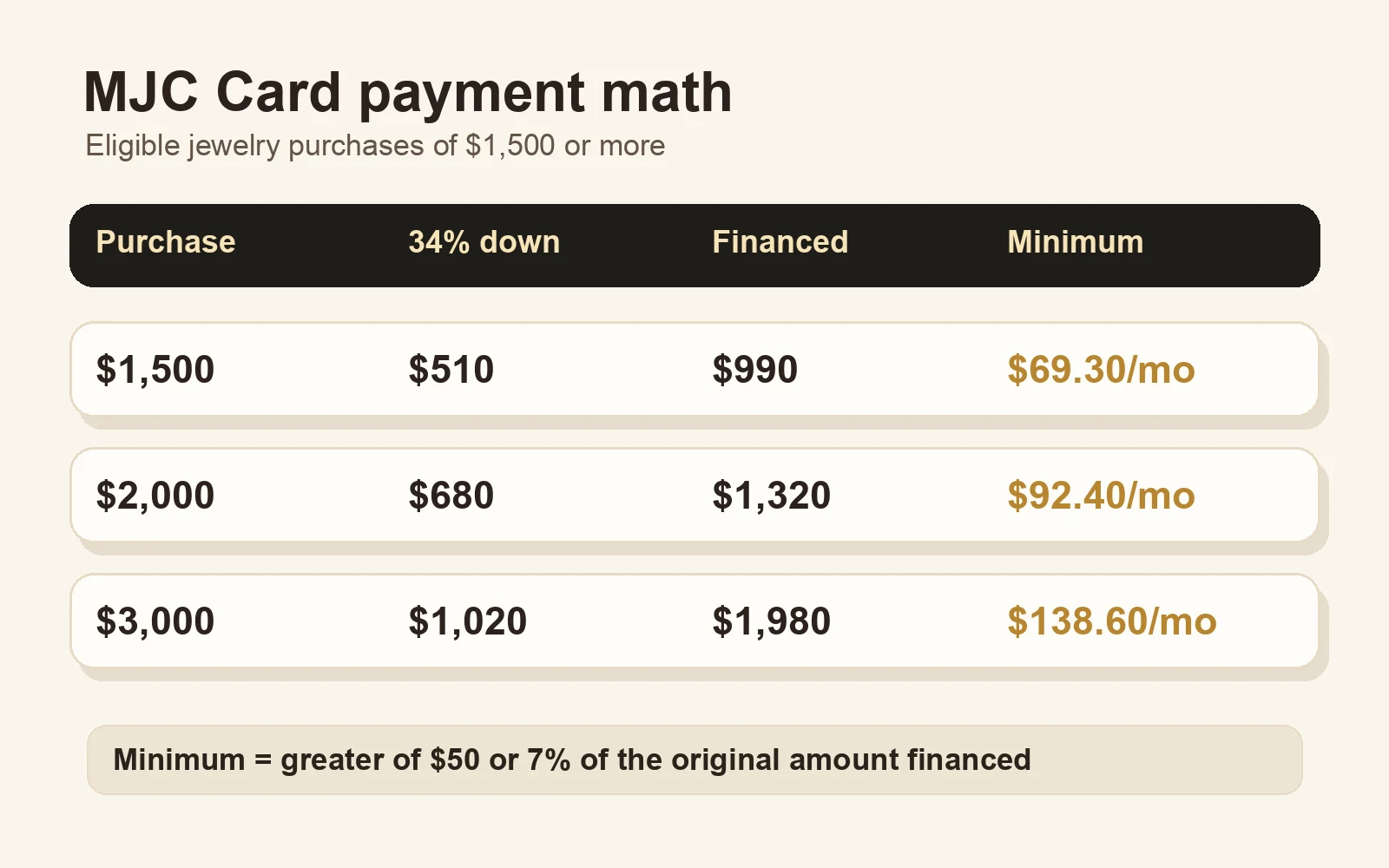

Buy Now Pay Later Jewelry Payment Math

Here is what the MJC Card looks like at three jewelry purchase prices. The down payment is 34% of the purchase, and the first minimum payment is the greater of $50 or 7% of the original amount financed:

| Purchase price | 34% down | Amount financed | Minimum monthly payment |

|---|---|---|---|

| $1,500 | $510 | $990 | $69.30 |

| $2,000 | $680 | $1,320 | $92.40 |

| $3,000 | $1,020 | $1,980 | $138.60 |

Interest accrues at 19.90% APR on the carried balance. The practical takeaway is simple: use the minimum to confirm the plan fits your monthly budget, then pay extra whenever you can. For the broader hub, see jewelry financing; for offer-specific plan wording, see jewelry payment plans.

Shop Jewelry You Can Buy Now and Pay Later

The MJC Card applies to eligible jewelry purchases of $1,500 or more. The product rail below is filtered to show finance-eligible pieces above that minimum:

Browse by category: engagement and wedding rings, rings, necklaces and pendants, earrings, bracelets, and men’s jewelry.

Buy Now Pay Later Engagement Rings

Buy now pay later engagement rings need more care than a small fashion-jewelry purchase because the balance is usually larger and the decision is emotional. A short Pay-in-4 option can work if you already have the cash flow to clear the balance quickly. For a ring you want to pay down over a longer period, the MJC Card gives you a fixed minimum payment, application-based eligibility and monthly payment activity reported monthly to credit bureaus.

For ring-specific math and denial-path guidance, use the engagement ring financing page. For month-by-month payoff examples, use the informational engagement ring monthly payments guide. If credit history is the concern, start with the best engagement rings for bad credit guide.

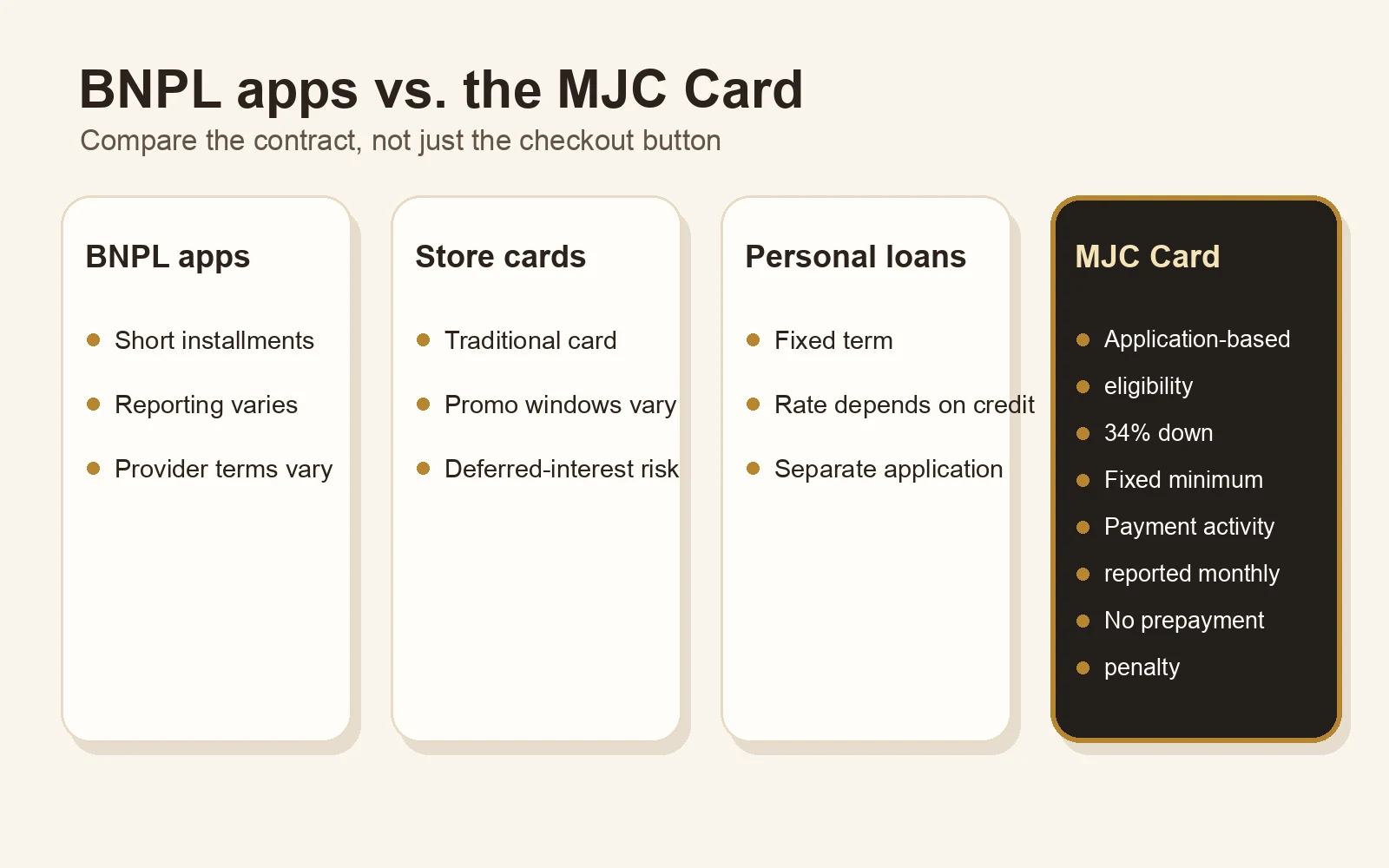

BNPL Apps vs. the MJC Card

BNPL apps often approve quickly and split the purchase into a short installment schedule. Many short-term plans are interest-free when every payment lands on time, but terms vary by provider and product. Some BNPL products do not report on-time payments to credit bureaus, so months of perfect payments may not support your payment history. The Consumer Financial Protection Bureau’s BNPL market report is a useful neutral reference for how the category works.

Store cards may offer promotional windows, but they usually depend on traditional credit-card underwriting and separate issuer terms. Deferred-interest promotions also require discipline: if the balance is not cleared by the deadline, the cost can change sharply. The deferred-interest jewelry financing guide explains that risk.

The MJC Card is designed for a different shopper: someone who wants to buy jewelry now, review clear terms before applying, make a predictable fixed minimum payment, and have payment activity reported monthly to credit bureaus. Approval is not guaranteed, and no score outcome can be promised, but the account structure is easier to understand before you commit.

No Credit Check Buy Now Pay Later Jewelry

If you are comparing no-credit-check buy now pay later jewelry offers, read the wording carefully. “No credit check” does not mean every applicant is approved, and “no credit needed” can describe a lease-to-own product rather than a credit account. Monetary Jewelers uses application-based eligibility for the MJC Card. For the terminology split, see no credit check vs. no credit needed jewelry financing.

How to Apply

The application takes a few minutes and works the same for eligible jewelry purchases of $1,500 or more:

- Apply online through the MJC Card application page.

- Receive your eligibility decision. Eligibility is application-based.

- Choose your jewelry, pay 34% down, and take it home.

- Make the fixed minimum payment or more each month; payment activity is reported monthly to credit bureaus.

Frequently Asked Questions

Can you buy jewelry now and pay later?

Yes. At Monetary Jewelers, the MJC Card lets eligible shoppers buy jewelry now and pay over time with 34% down, 19.90% APR, and a fixed minimum monthly payment of $50 or 7% of the original amount financed, whichever is greater.

Is buy now pay later jewelry the same as financing?

It depends on the product. Some BNPL apps are short installment plans, while the MJC Card is an in-house revolving credit account. The important questions are whether interest can accrue, how the payment is calculated, how eligibility is decided, and whether payment activity is reported.

Can you get buy now pay later engagement rings with no credit check?

With the MJC Card, engagement ring eligibility is application-based rather than tied to a single score cutoff. Approval is not guaranteed, so review the terms before using the account.

What is the monthly payment on $1,500 of buy now pay later jewelry?

With the MJC Card: $510 down (34%), $990 financed, and a minimum monthly payment of $69.30, the greater of $50 or 7% of the original amount financed. Paying more than the minimum shortens the payoff with no prepayment penalty.

Do BNPL jewelry apps build credit?

Some products may report, but many short-term BNPL plans do not report on-time payments to credit bureaus. If payment-history reporting matters to you, confirm the exact product before relying on it. MJC Card payment activity is reported monthly to credit bureaus.

Can you pay off the MJC Card early?

Yes. There is no prepayment penalty. Paying more than the fixed minimum can reduce total interest and shorten the payoff timeline.