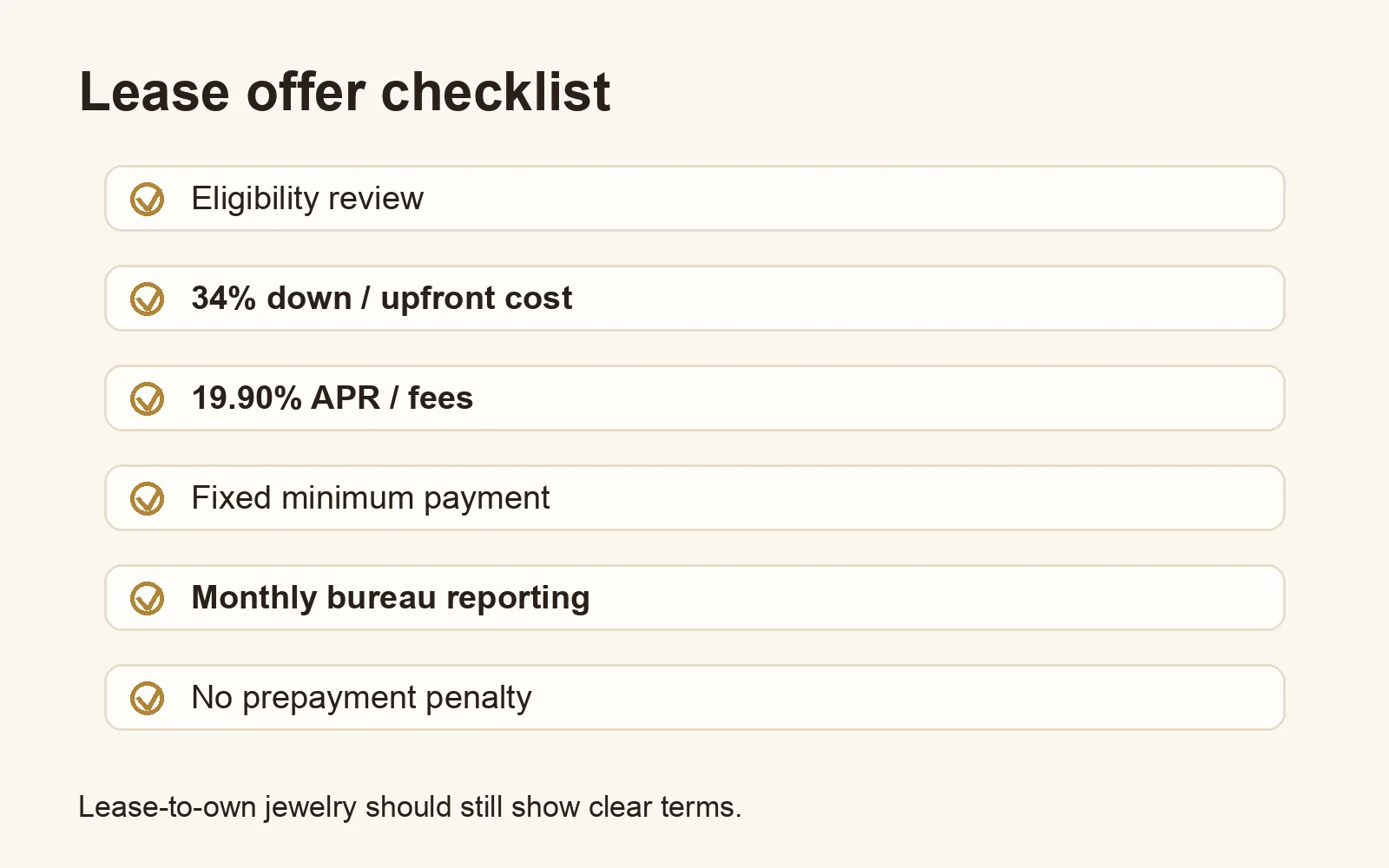

Lease-to-own jewelry and rent-to-own jewelry offers promise a way to take home an engagement ring, wedding band, gold chain, or fine-jewelry piece and pay over time. The label is handy, but it gets confused with store financing, personal loans, buy-now-pay-later apps, and in-house credit accounts. Monetary Jewelers does not offer the MJC Card as a lease-to-own contract. The MJC Card is an in-house revolving credit account for jewelry purchases, with application-based eligibility, 34% down, 19.90% APR, a fixed minimum-payment formula, no prepayment penalty, and payment activity is reported monthly to credit bureaus.

If you are comparing lease-style offers against store financing, see jewelry stores that finance for the MJC Card terms and checklist.

What Lease-to-Own Jewelry Means

Lease-to-own jewelry usually means you make scheduled payments under a lease or rental-style agreement, then own the item after you finish the required payments or use a purchase option. Search results often use “rent-to-own jewelry” to mean the same thing. The details matter. Ownership timing, fees, payment frequency, early-purchase rules, late-payment terms, and whether the account reports payment activity can all vary widely from one offer to the next.

Before choosing a lease-to-own jewelry offer, ask these questions:

- When do I legally own the jewelry?

- What is the total cost if I make every scheduled payment?

- Is there an early purchase option or payoff discount?

- Does the offer report payment activity monthly to credit bureaus?

- What happens if a payment is late?

- Is this a lease, a loan, a BNPL plan, or a credit account?

Lease-to-Own Jewelry vs. MJC Card Financing

The MJC Card is not lease-to-own jewelry and not a rent-to-own contract. It is an in-house revolving credit account that can be used for Monetary Jewelers purchases. The core terms are:

- Application-based eligibility

- Minimum jewelry purchase for MJC Card financing is $1,500

- 34% down

- 19.90% APR

- Minimum monthly payment of $50 or 7% of the original amount financed, whichever is greater

- No prepayment penalty

- Payment activity is reported monthly to credit bureaus

- Approval is not guaranteed

That gives shoppers a clear alternative to lease-to-own jewelry. Instead of decoding rental ownership rules, you can look at a set down payment, an APR, a minimum payment formula, how the account reports, and what early payoff costs. If you are weighing several payment categories, also see jewelry payment plans, buy now pay later jewelry, and jewelry loans.

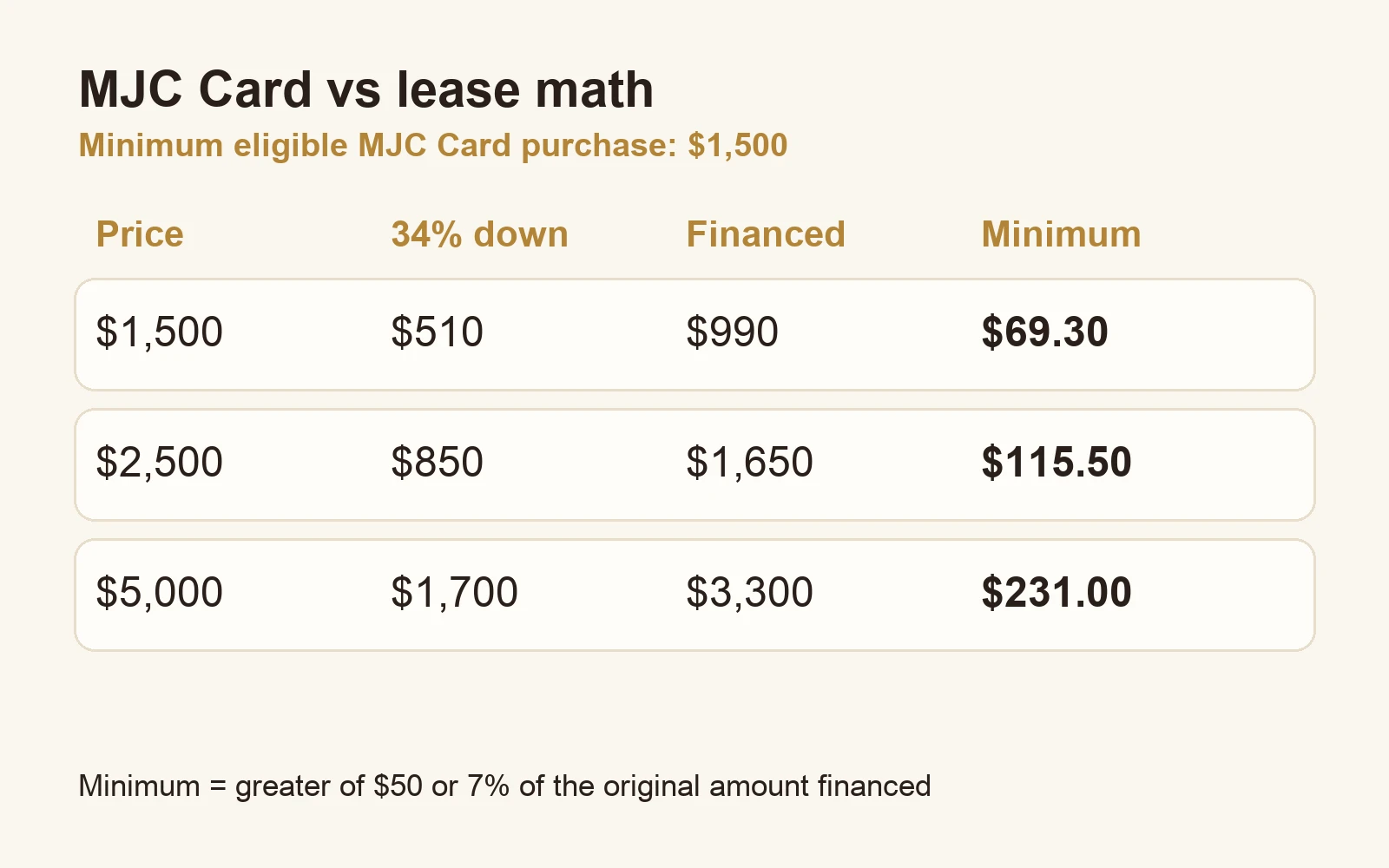

Payment Examples

Here is what the MJC Card payment structure looks like at three common jewelry purchase prices. The down payment is 34% of the purchase, and the minimum monthly payment is the greater of $50 or 7% of the original amount financed:

| Purchase price | 34% down | Amount financed | Minimum monthly payment |

|---|---|---|---|

| $1,500 | $510 | $990 | $69.30 |

| $2,500 | $850 | $1,650 | $115.50 |

| $5,000 | $1,700 | $3,300 | $231.00 |

Interest accrues at 19.90% APR on any carried balance. There is no prepayment penalty, so paying more than the minimum can reduce total interest and shorten the payoff timeline. For the broader financing hub, see jewelry financing; for ring-specific planning, see engagement ring financing.

Shop Jewelry You Can Finance

MJC Card eligibility can be considered for eligible jewelry purchases of $1,500 or more. Popular finance-eligible pieces above that minimum:

Browse by category: engagement and wedding rings, rings, necklaces and pendants, earrings, bracelets, and men’s jewelry.

How to Compare Lease-to-Own and Rent-to-Own Jewelry Offers

Start with ownership. A lease-to-own offer may not transfer ownership until the end of the agreement. If you want to own the jewelry immediately after purchase, verify that the product you are considering is not actually a rental-style contract.

Compare total cost, not just the weekly payment. Lease-to-own jewelry can advertise small weekly or monthly payments while the total of payments is much higher than the ticket price. Compare the full cost against alternatives before signing.

Check reporting behavior. If payment-history reporting matters to you, confirm whether the account reports payment activity. MJC Card payment activity is reported monthly to credit bureaus. On-time payments can support payment history over time; late payments can hurt it.

Look for early-payoff flexibility. The MJC Card has no prepayment penalty. Lease-to-own agreements may use different early-purchase rules, so read that section carefully.

Lease-to-Own Jewelry Online or Near Me

People who search “lease-to-own jewelry online” or “lease-to-own jewelry near me” usually want a piece they can buy now with a payment structure that does not feel like a bank loan. The safest way to compare is product by product. A local rent-to-own jeweler, a national BNPL app, a personal loan, and the MJC Card each handle the cash-flow problem differently.

If you are weighing Monetary Jewelers against lease-to-own jewelry stores, the MJC Card is a jewelry-specific account with application-based eligibility, 34% down, 19.90% APR, a fixed minimum payment, no prepayment penalty, and payment activity reported monthly to credit bureaus. If credit-check wording is part of your search, the no credit check jewelry financing guide is a useful companion page.

When the MJC Card May Fit Better

The MJC Card may fit better than lease-to-own jewelry when you want clear credit-account terms, monthly reporting, and the ability to pay early without a prepayment penalty. It will not fit every shopper. Approval is not guaranteed, 34% down is required, and the account is for Monetary Jewelers purchases rather than general cash.

If you are choosing between options, start with the contract type, then look at the down payment, APR or fees, monthly payment, ownership timing, how the account reports, and payoff flexibility. That tells you more than the label “lease-to-own” alone.

How to Apply for the MJC Card

The MJC Card application path is straightforward:

- Apply online through the MJC Card application page.

- Receive an eligibility decision; eligibility is application-based.

- If approved, choose your jewelry and pay 34% down.

- Finance the remaining balance at 19.90% APR with a minimum monthly payment of $50 or 7% of the original amount financed, whichever is greater.

- Pay the fixed minimum or more each month; there is no prepayment penalty, and payment activity is reported monthly to credit bureaus.

Frequently Asked Questions

Does Monetary Jewelers offer lease-to-own jewelry?

No. Monetary Jewelers offers MJC Card financing, not a lease-to-own contract. The MJC Card is an in-house revolving credit account for jewelry purchases.

Is lease-to-own jewelry the same as financing?

Not always. Lease-to-own jewelry is usually a rental or lease-style agreement with ownership after required payments or a purchase option. Financing can also refer to credit accounts, BNPL plans, or personal loans.

What are the MJC Card terms?

The MJC Card uses application-based eligibility, 34% down, 19.90% APR, and a minimum monthly payment of $50 or 7% of the original amount financed, whichever is greater. There is no prepayment penalty.

Does the MJC Card report payments?

Yes. MJC Card payment activity is reported monthly to credit bureaus. On-time payments can support payment history over time, while late payments can hurt it. No credit-score outcome can be promised.

What is the payment on $2,500 of jewelry?

With the MJC Card, a $2,500 purchase has $850 down, $1,650 financed, and a minimum monthly payment of $115.50.

Can I pay off MJC Card financing early?

Yes. The MJC Card has no prepayment penalty. Paying more than the minimum can reduce total interest and shorten the payoff timeline.