Engagement ring financing lets you take the ring home now and pay for it over fixed monthly payments instead of paying everything upfront. At Monetary Jewelers, financing runs on the MJC Card, our in-house revolving credit account with application-based eligibility and clear terms before you apply. This page covers the exact terms, the payment math on rings at different prices, how the MJC Card compares to BNPL and personal loans, and how to apply.

How Engagement Ring Financing Works at Monetary Jewelers

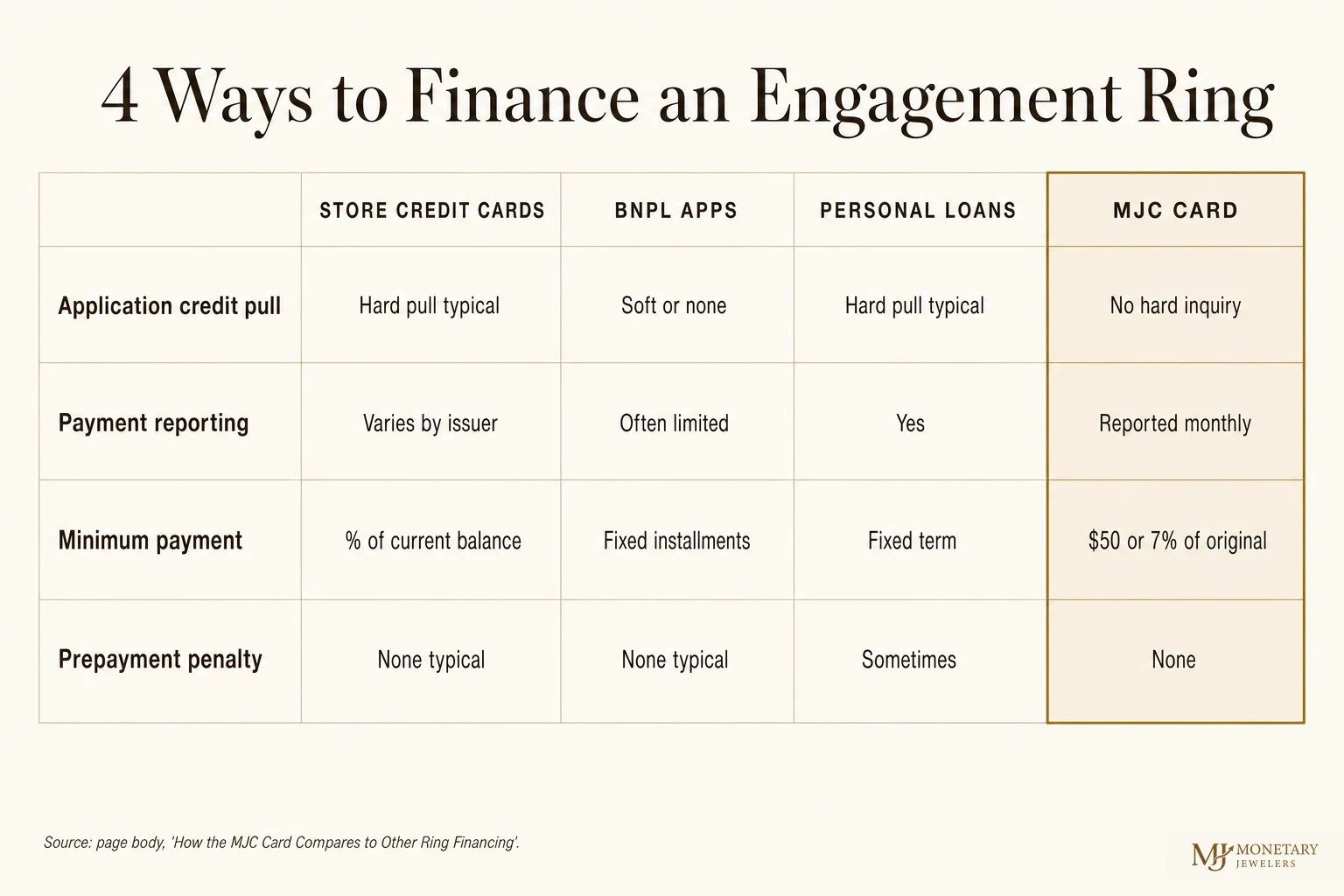

Most ring financing falls into four buckets: retailer credit accounts, buy-now-pay-later installment plans, personal loans, and general-purpose credit cards. Each differs in how interest accrues, how the minimum payment is calculated, whether payment history reaches the credit bureaus, and what the application does to your credit file.

The MJC Card is the first kind. It is a revolving account issued directly by Monetary Jewelers, with application-based eligibility instead of a traditional credit-score cutoff. The MJC Card terms:

- Application-based eligibility

- Minimum jewelry purchase for MJC Card financing is $1,500

- 34% down

- 19.90% APR

- Minimum monthly payment of $50 or 7% of the original amount financed, whichever is greater

- No prepayment penalty

- Monthly payment activity is reported monthly to credit bureaus

Two of those terms do most of the work. The minimum payment is calculated against the original amount financed, not the declining balance, so the number you budget for in month one is the same number through payoff. And because there is no prepayment penalty, paying more than the minimum shortens the payoff and reduces total interest with no downside.

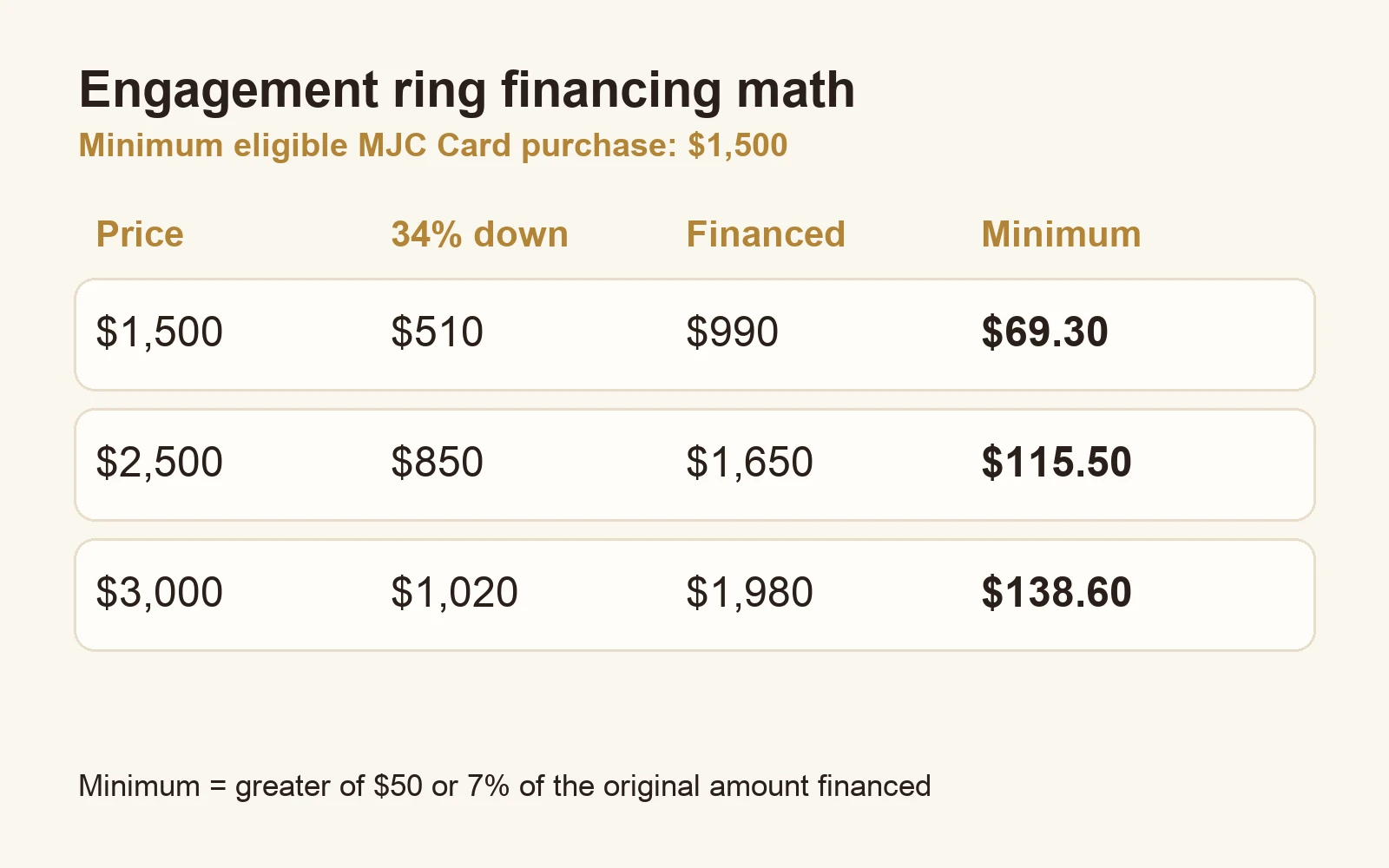

The Payment Math on Real Rings

Here is what the MJC Card structure looks like at three common price points. The down payment is 34% of the purchase, and the first minimum payment is the greater of $50 or 7% of the amount financed:

| Ring price | 34% down | Amount financed | Minimum monthly payment |

|---|---|---|---|

| $1,500 | $510 | $990 | $69.30 |

| $2,500 | $850 | $1,650 | $115.50 |

| $3,000 | $1,020 | $1,980 | $138.60 |

Interest accrues at 19.90% APR on the carried balance, so the fastest way to lower the total cost is paying above the minimum. For month-by-month breakdowns at more price points, see the engagement ring monthly payments guide.

Shop Engagement Rings You Can Finance

MJC Card financing is available for eligible ring purchases of $1,500 or more. Start with popular engagement styles above that minimum:

Browse the full engagement and wedding rings collection, or compare across all ring styles.

How the MJC Card Compares to Other Ring Financing

Buy-now-pay-later plans split one purchase into short-term installments. Many are interest-free if every payment lands on time, but some BNPL providers do not report on-time payments to the credit bureaus, so months of perfect payments can add nothing to your payment history. Promotional windows are the other catch: with deferred-interest offers, carrying any balance past the deadline can trigger the full accumulated interest at once. The deferred-interest guide walks through that math, and the Affirm vs. Klarna vs. Afterpay comparison covers the major BNPL options for rings, with the Consumer Financial Protection Bureau’s deferred-interest explainer as a neutral reference.

Personal loans offer fixed terms and rates that depend on your credit profile, but the application typically involves a hard inquiry, and strong rates generally require strong credit.

General-purpose credit cards recalculate the minimum as a percentage of the current balance, so the payment shrinks while the payoff stretches.

The MJC Card trades differently: application-based eligibility, a predictable fixed minimum, and monthly payment activity reported to credit bureaus. On-time payments can support your payment history over time, and late payments can hurt it.

Financing a Wedding Ring or Bridal Set

Wedding ring financing uses the same MJC Card terms when the eligible purchase is $1,500 or more, whether you finance an engagement ring, a wedding band, or a bridal set together. If credit history is the concern, start with the best engagement rings for bad credit guide.

Denied for Ring Financing Before?

A past denial from a bank card or BNPL provider does not decide the outcome here. The MJC Card uses application-based eligibility rather than a score cutoff and uses application-based eligibility rather than a traditional score cutoff. If you have been turned down recently, the engagement ring financing after denial guide covers what denials actually mean and the practical next steps.

How to Apply

The application takes a few minutes and shows terms before you decide whether to use the account:

- Apply online through the MJC Card application page.

- Receive your eligibility decision. Eligibility is application-based.

- Pick your ring, pay 34% down, and take it home.

- Make the fixed minimum payment (or more) each month; payment activity is reported monthly to credit bureaus.

Frequently Asked Questions

Can you finance an engagement ring with no credit check?

The MJC Card uses application-based eligibility rather than a minimum credit-score cutoff. Approval is not guaranteed for any financing product, so read the terms before deciding whether to use the account.

What credit score do you need to finance an engagement ring?

With the MJC Card, there is no minimum-score requirement because eligibility is application-based. Lenders that use score cutoffs vary widely. The credit score guide explains how different financing types evaluate applicants.

What is the monthly payment on a $3,000 engagement ring?

With the MJC Card: $1,020 down (34%), $1,980 financed, and a minimum monthly payment of $138.60, the greater of $50 or 7% of the original amount financed. The minimum stays the same through payoff, and paying more than the minimum shortens it with no prepayment penalty.

Can you finance a wedding ring the same way?

Yes. Wedding ring financing uses the same MJC Card terms: 34% down, 19.90% APR, the fixed $50-or-7% minimum, and monthly reporting of payment activity to credit bureaus. Bands and bridal sets qualify the same as engagement rings.

Does financing an engagement ring build credit?

It can support your credit file if the account reports and you pay on time. MJC Card payment activity is reported monthly to credit bureaus, so on-time payments can support your payment history over time, and late payments can hurt it. No specific score outcome or timeline can be promised; results depend on your full credit profile.

What if I was denied jewelry financing before?

You can still apply. The MJC Card does not use a traditional score cutoff. Approval is still not guaranteed, so use the after-denial guide to understand what may have changed before you apply again. The after-denial guide covers why denials happen and what to do next.